RF Insights: July Market Update

Grayson Daniels, VP of Grain Sales and Procurement, breaks down the latest for rice and soybean markets.

Rice Fundamental Highlights

- The June 30 Acreage report showed significant long grain acreage reductions in line with expectations. U.S. long grain acres are down 34% compared to last year. Arkansas’ total rice acres are the lowest since 1977. Medium grain acres are up 16% in Arkansas, but down 14% in California.

- The JULY WASDE report increased old crop exports from 111 million bushels to 120 million bushels, and left imports and domestic use unchanged. Ending stocks decreased to 81.3 million bushels, slightly below the previous crop.

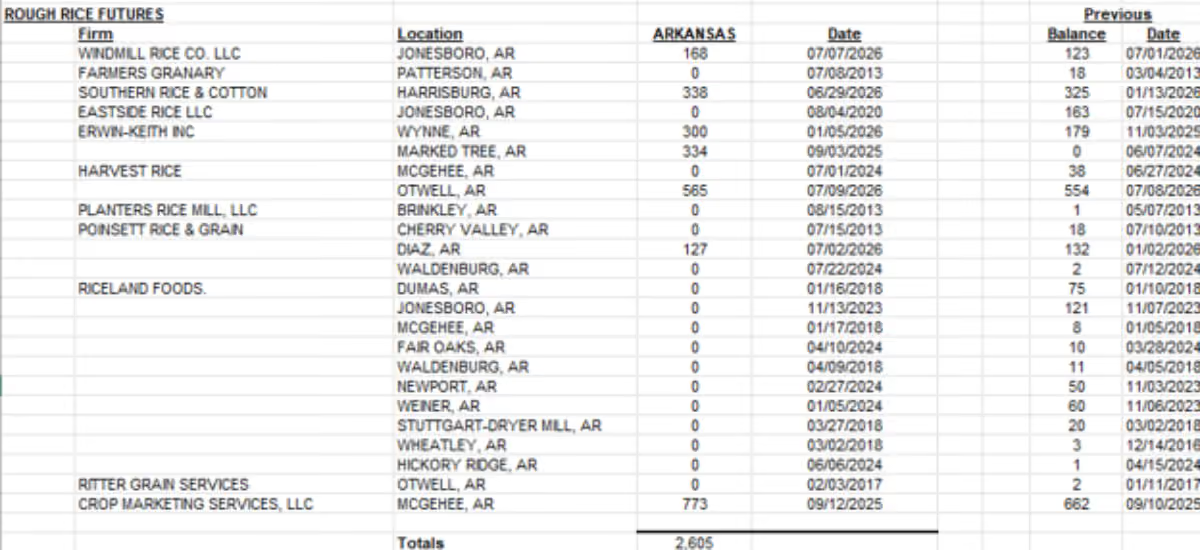

- CBOT certificates have climbed to 2605 on the July delivery cycle, a new record high. Large old crop stocks and a CBOT milling yield premium and discount schedule that is not reflective of the current trade is contributing to the record receipts.

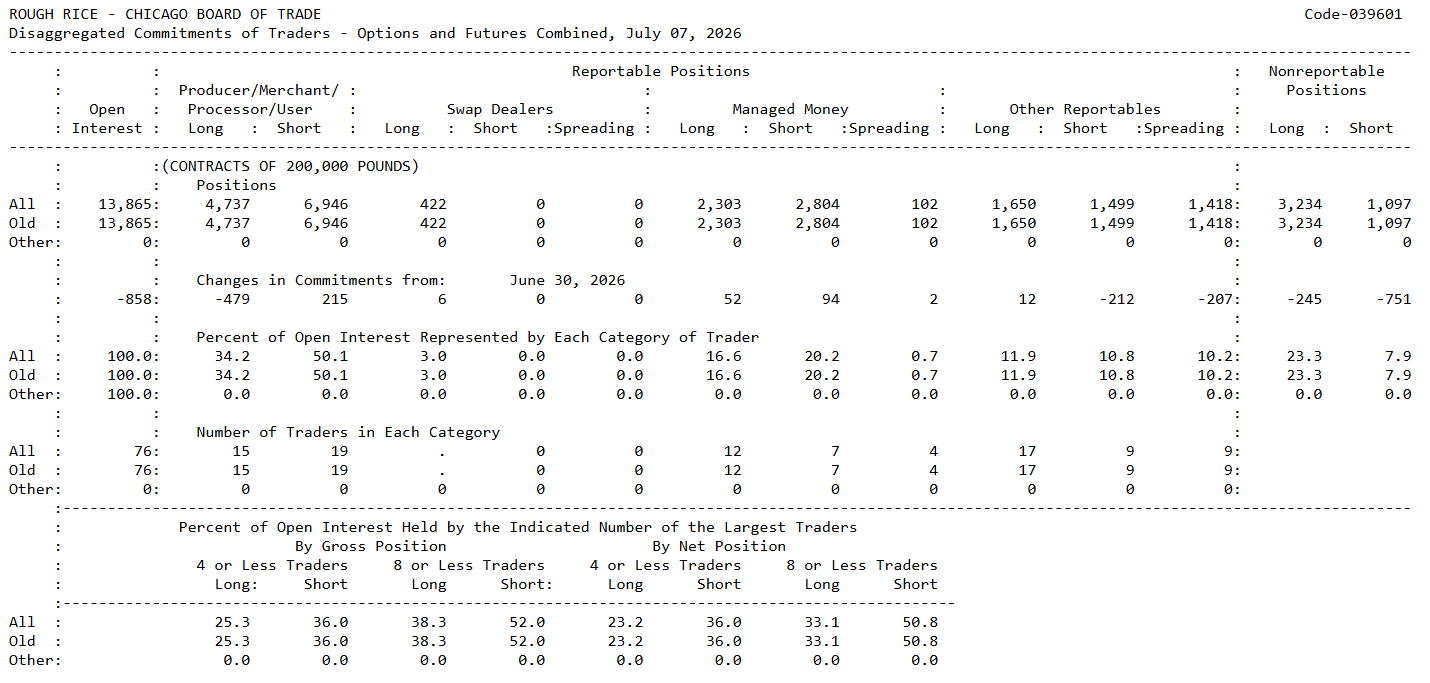

- CFTC Commitments of Traders show the fund segment about 500 contracts net short. The commercial segment is increasing their net short position with increased farmer selling. The mid level traders are evenly split between longs and shorts and the small traders are net long over 2,100 contracts.

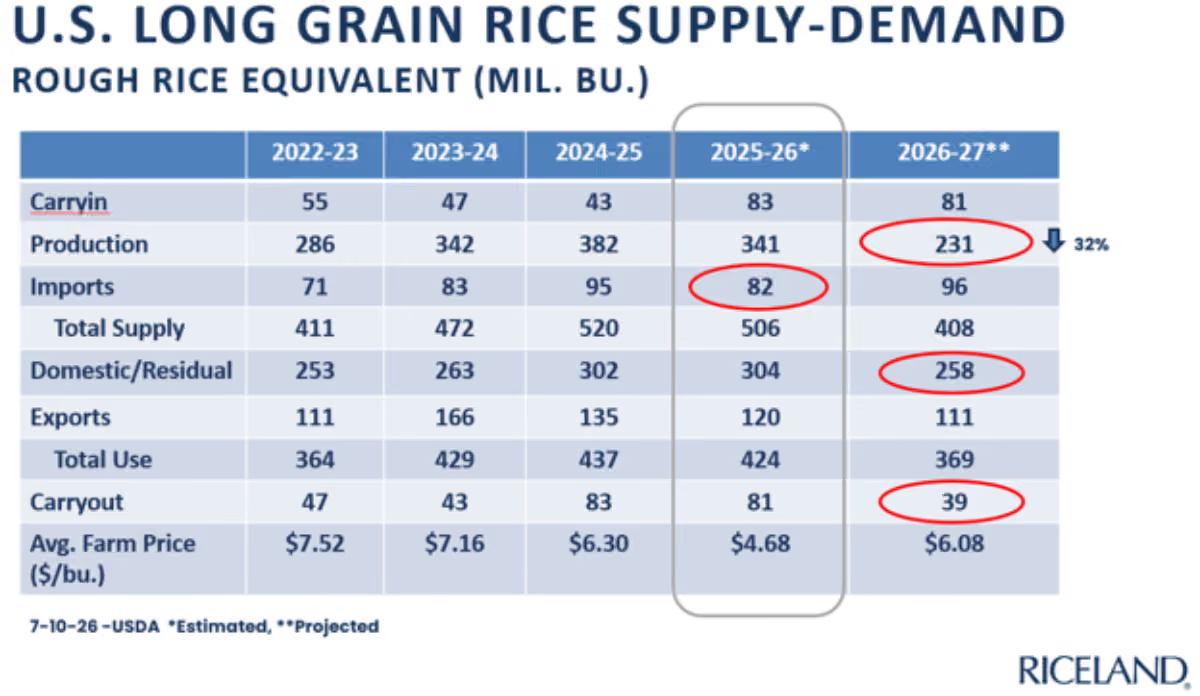

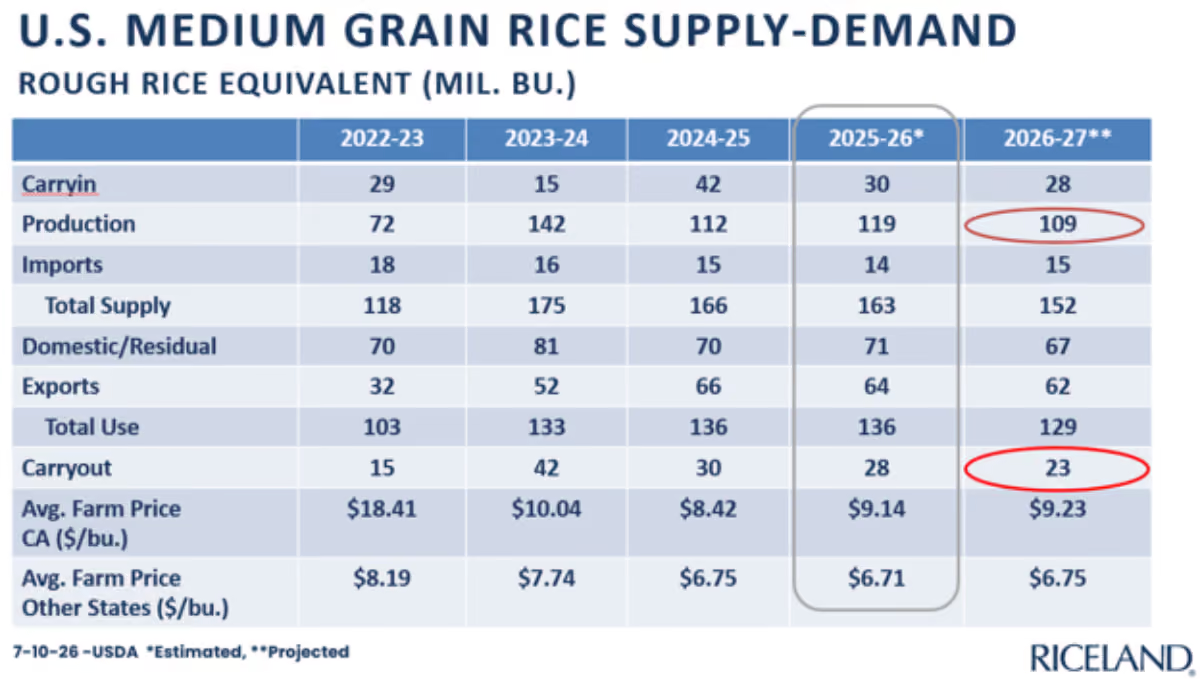

- USDA’s JULY WASDE incorporated the June 30 acres report and thus made substantial changes, including dropping production 41 million bushels. USDA cut the domestic use projection and increased imports to 96 million bushels, which would be a new record if realized.

- The projected ending stocks for the 2026/27 crop dropped to 39 million bushels, which would be an uncomfortably tight level of stocks. For comparison, the 2019/20 crop ending stocks were 37.6 million bushels.

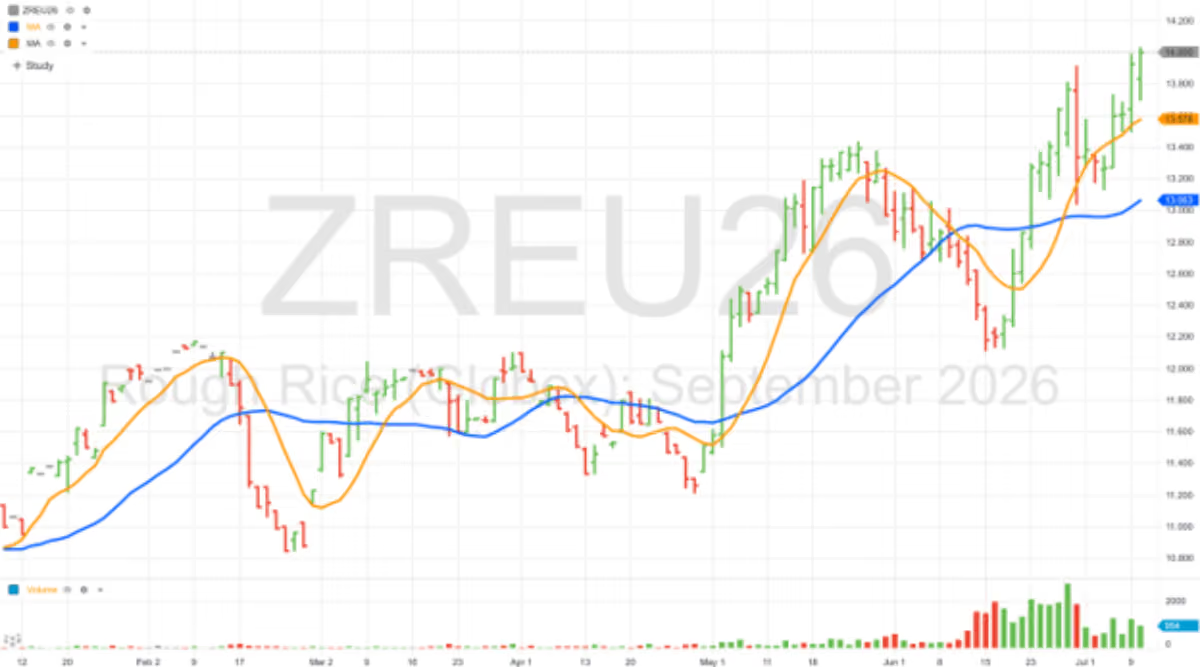

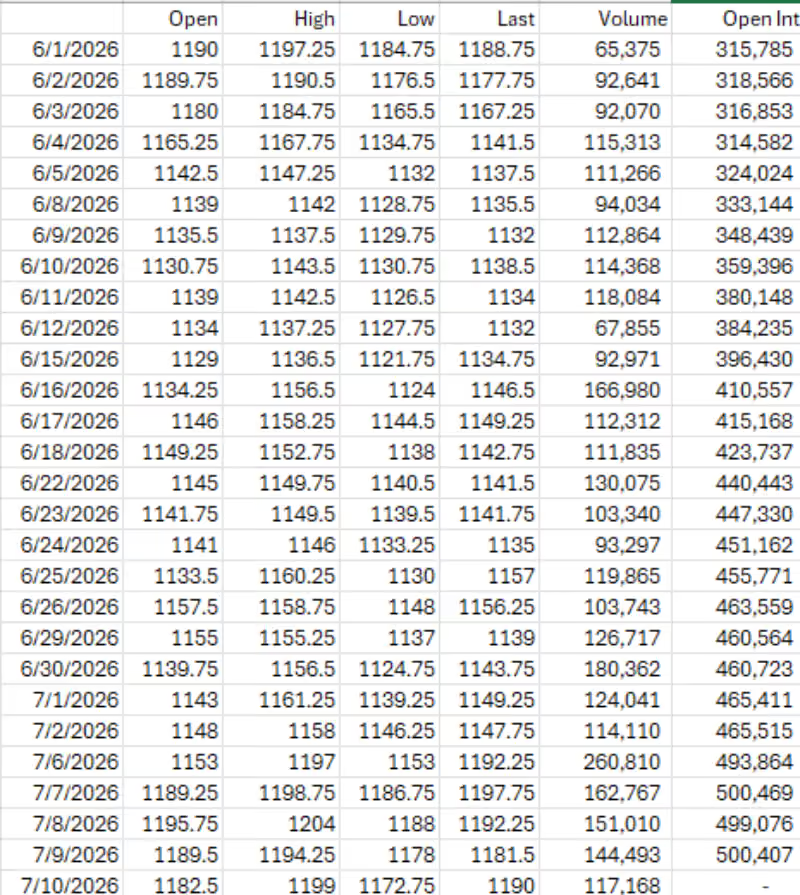

September ‘26 Rough Rice Futures

Orange Line = 9 day moving average

Blue Line = 27 day moving average

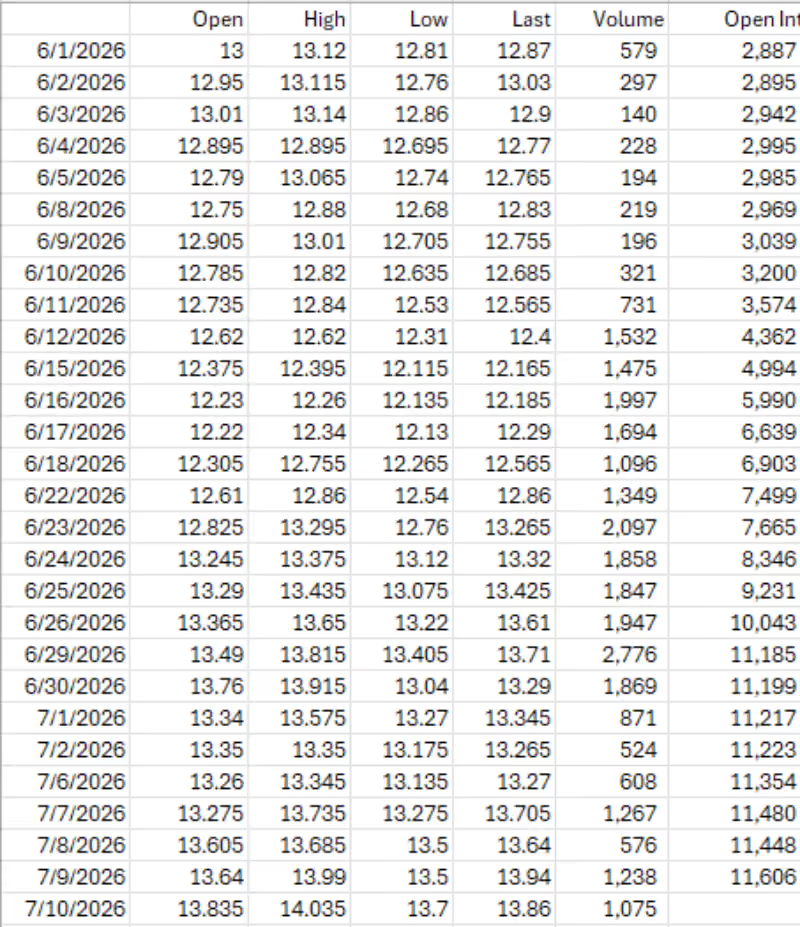

CBOT September ’26 Rough Rice Values, 6/1/26 through 7/10/26

CBOT Receipts As of 7-9-26

CFTC Commitments of Traders

Soybean Fundamental Highlights

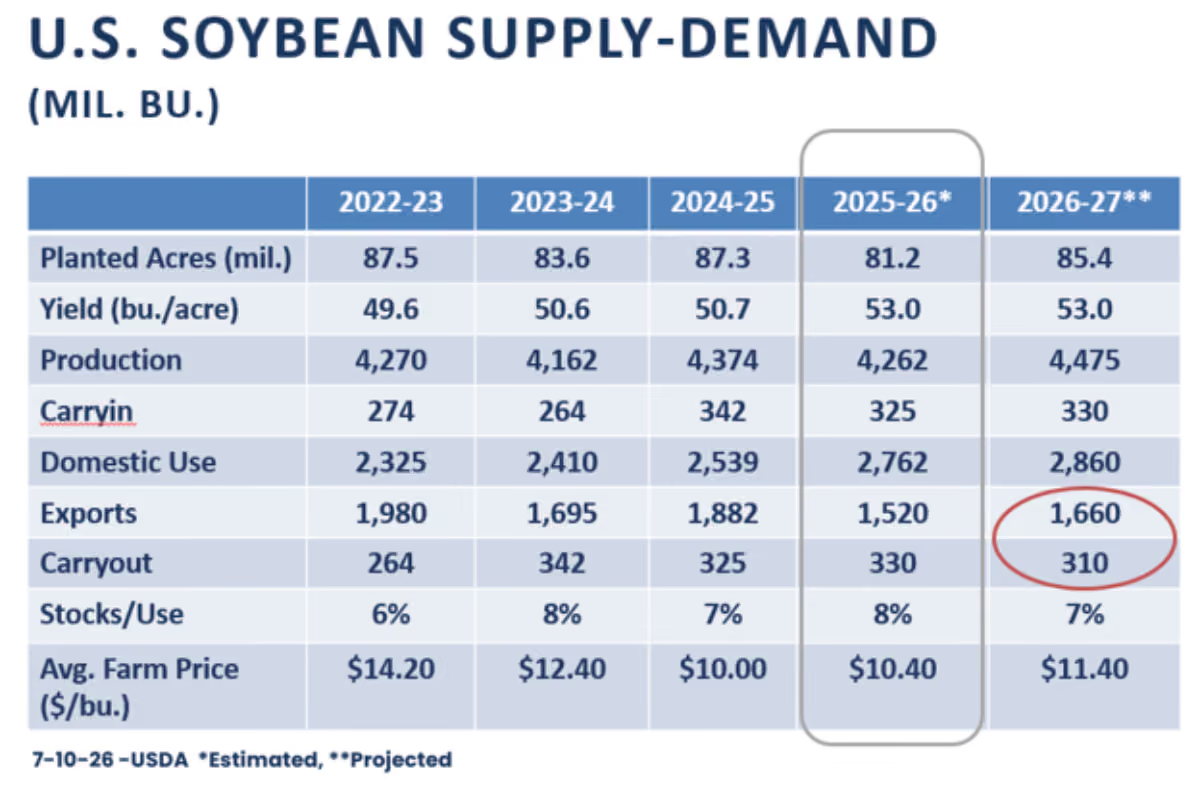

- The June 30 acreage report showed soybean acres at 85.4 million, a 4.2 million acre increase in plantings compared to 2025 and 665,000 higher than the March Prospective Plantings report.

- The JULY WASDE increased old crop exports 10 million bushels, resulting in ending stocks dropping to 330 million bushels.

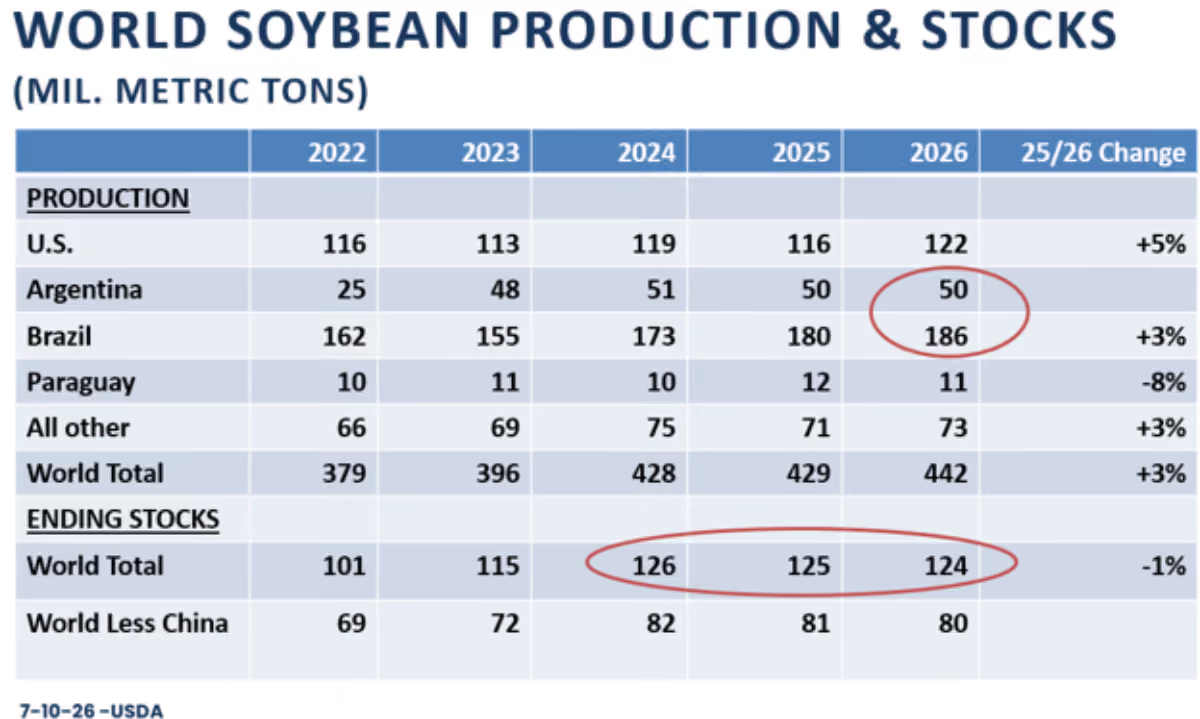

- The soybean market has seen a nice recovery in recent weeks as weather concerns increase in some areas and China has shown up to purchase U.S. soybeans once again.

- The JULY WASDE offset the increased new crop production with a decrease in beginning stocks and an increase in exports. Projected ending stocks remain at 310 million bushels.

- July and August weather and pace of China purchases will continue to drive the market during the last weeks of summer.

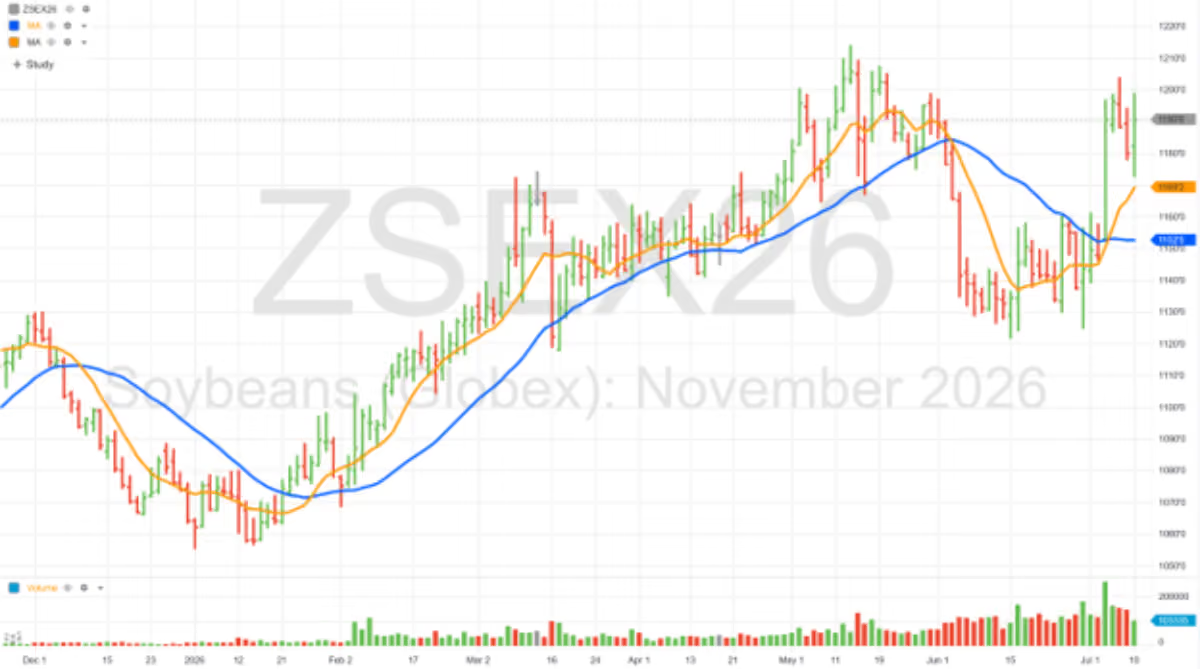

November ‘26 Soybean Futures

Orange Line = 9 day moving average

Blue Line = 27 day moving average

CBOT November ’26 Soybean Values, 6/1/26 through 7/10/26

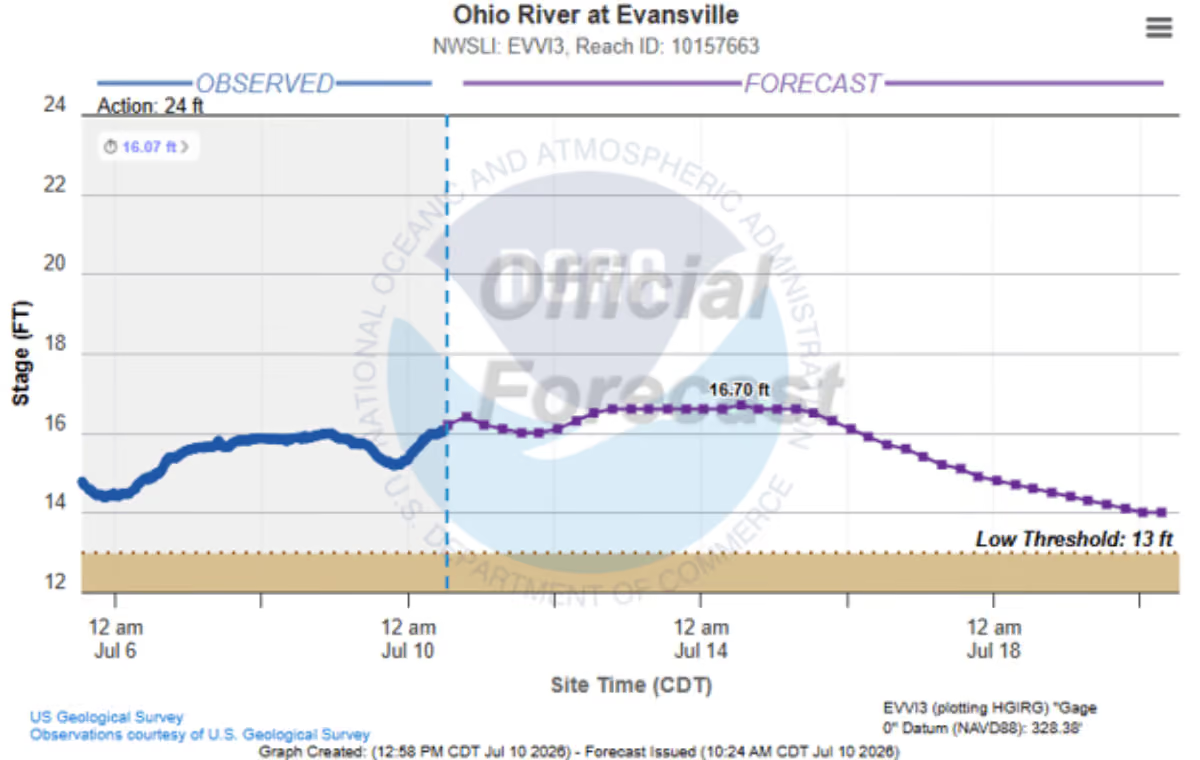

River / Weather

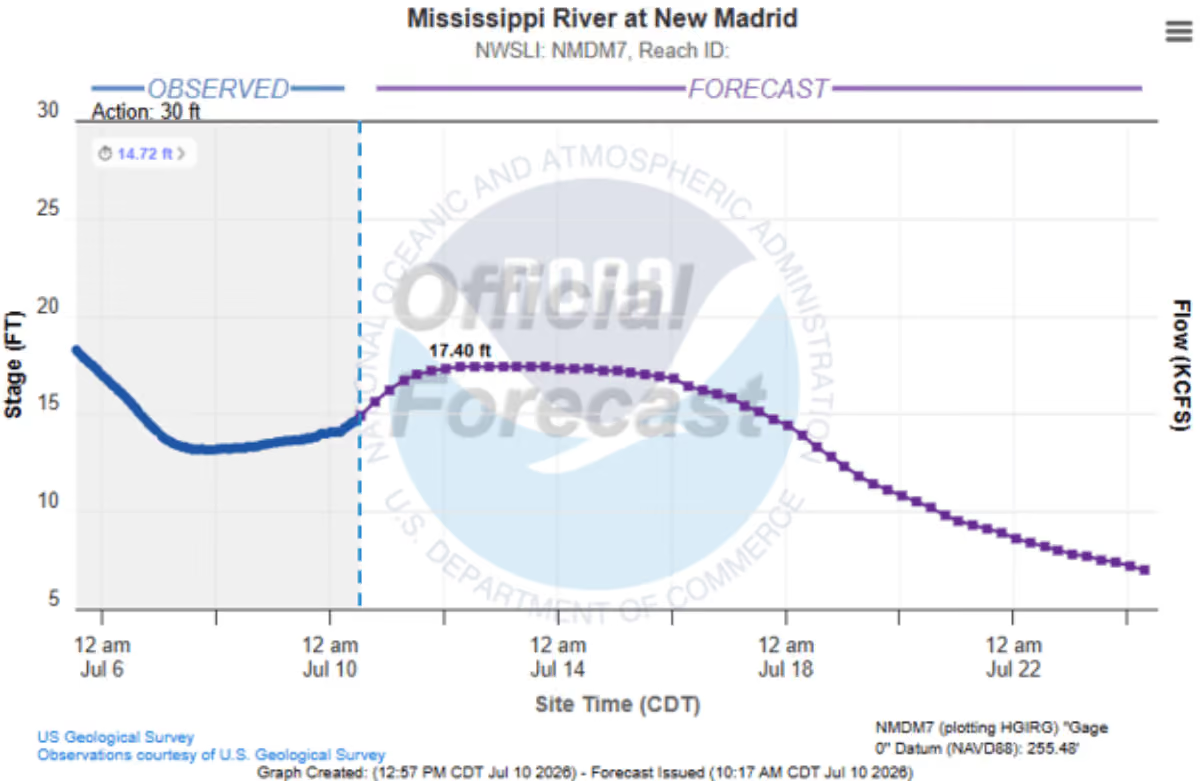

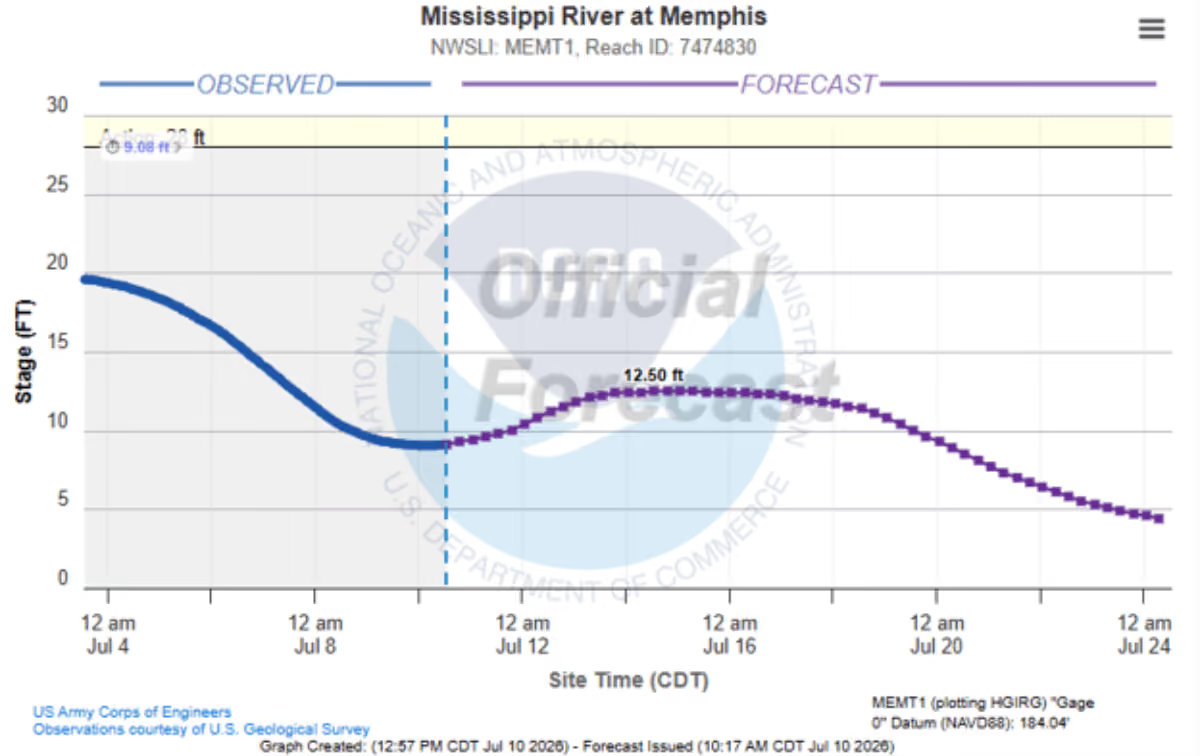

The Mississippi River graphs show ample water for navigation after recent rains; however, the river forecast drops significantly without continued rainfall. This is a concerning trend if we start missing rains in late July and August.

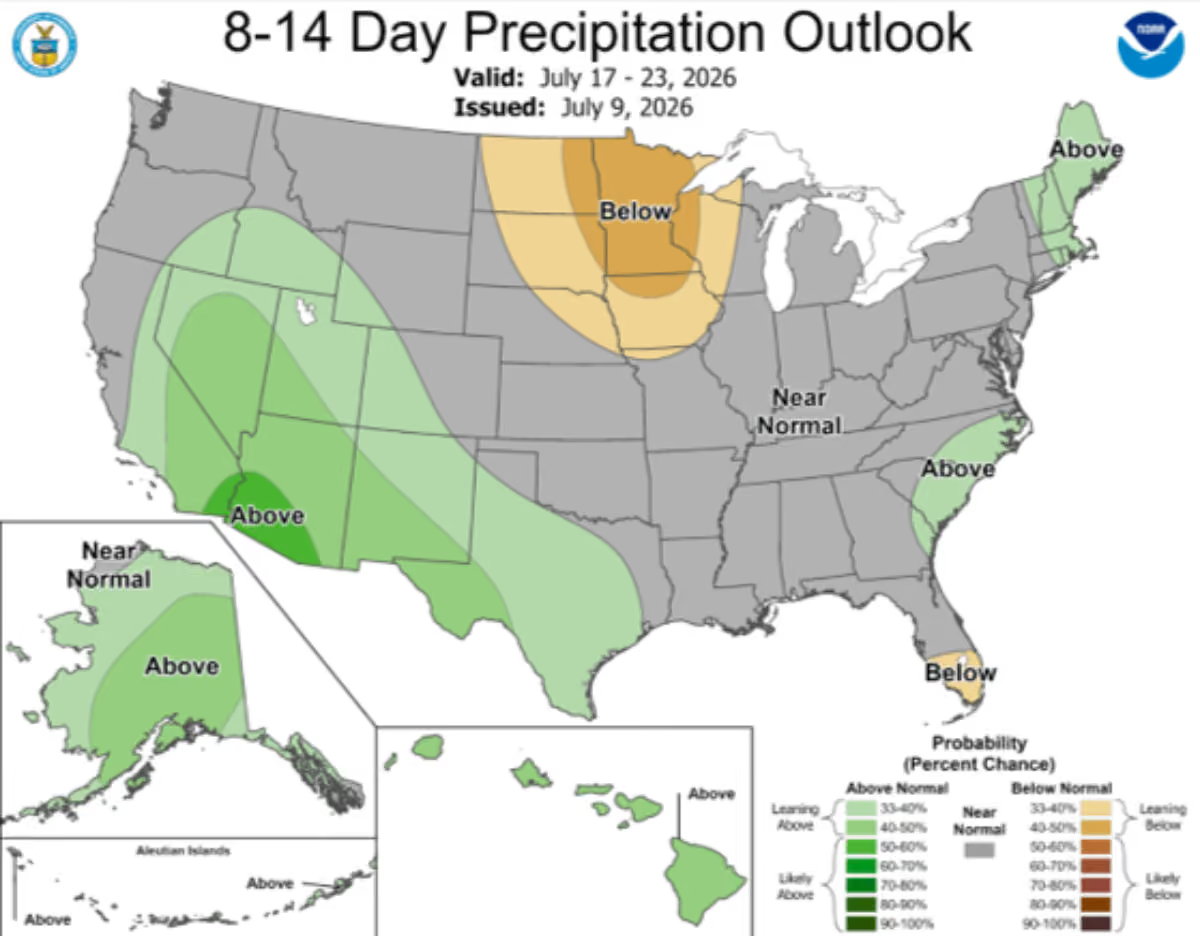

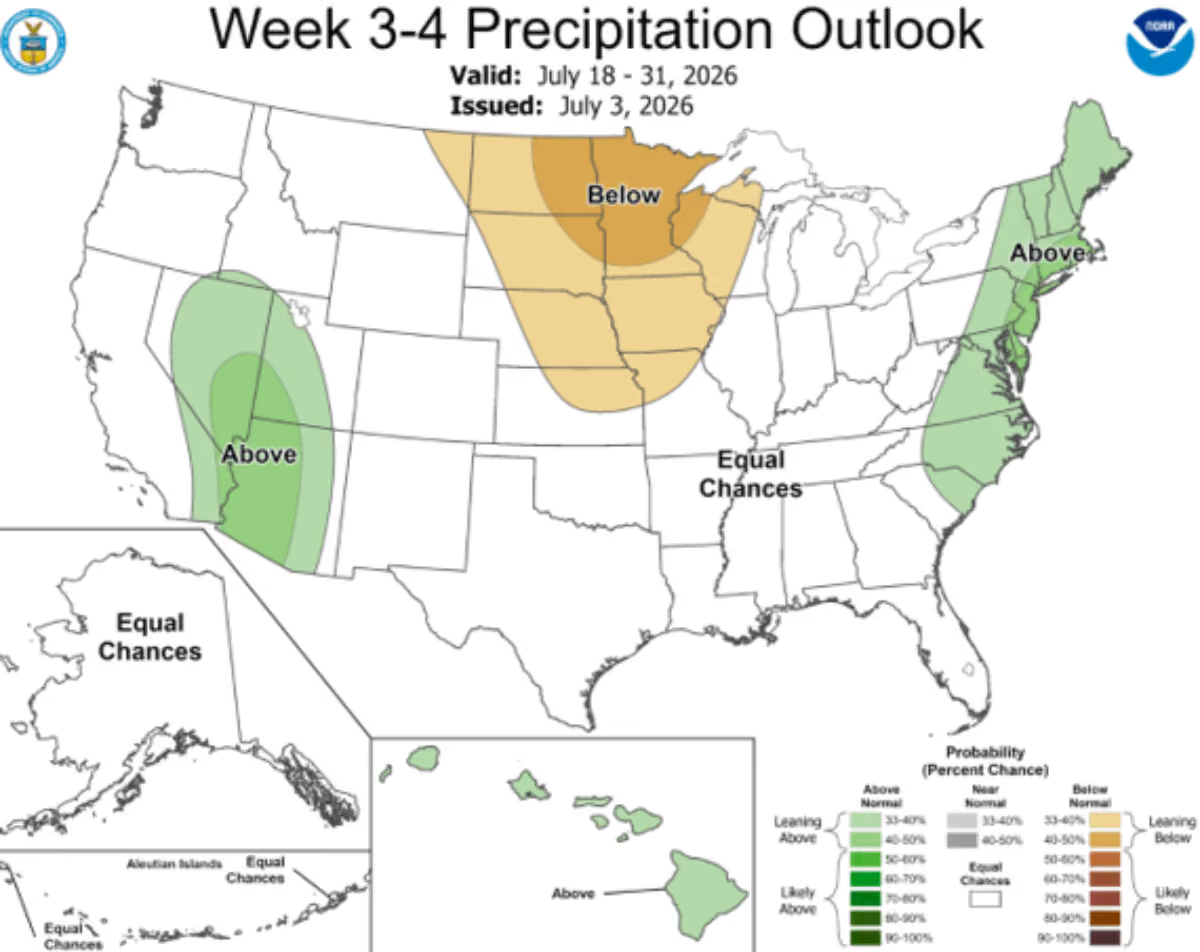

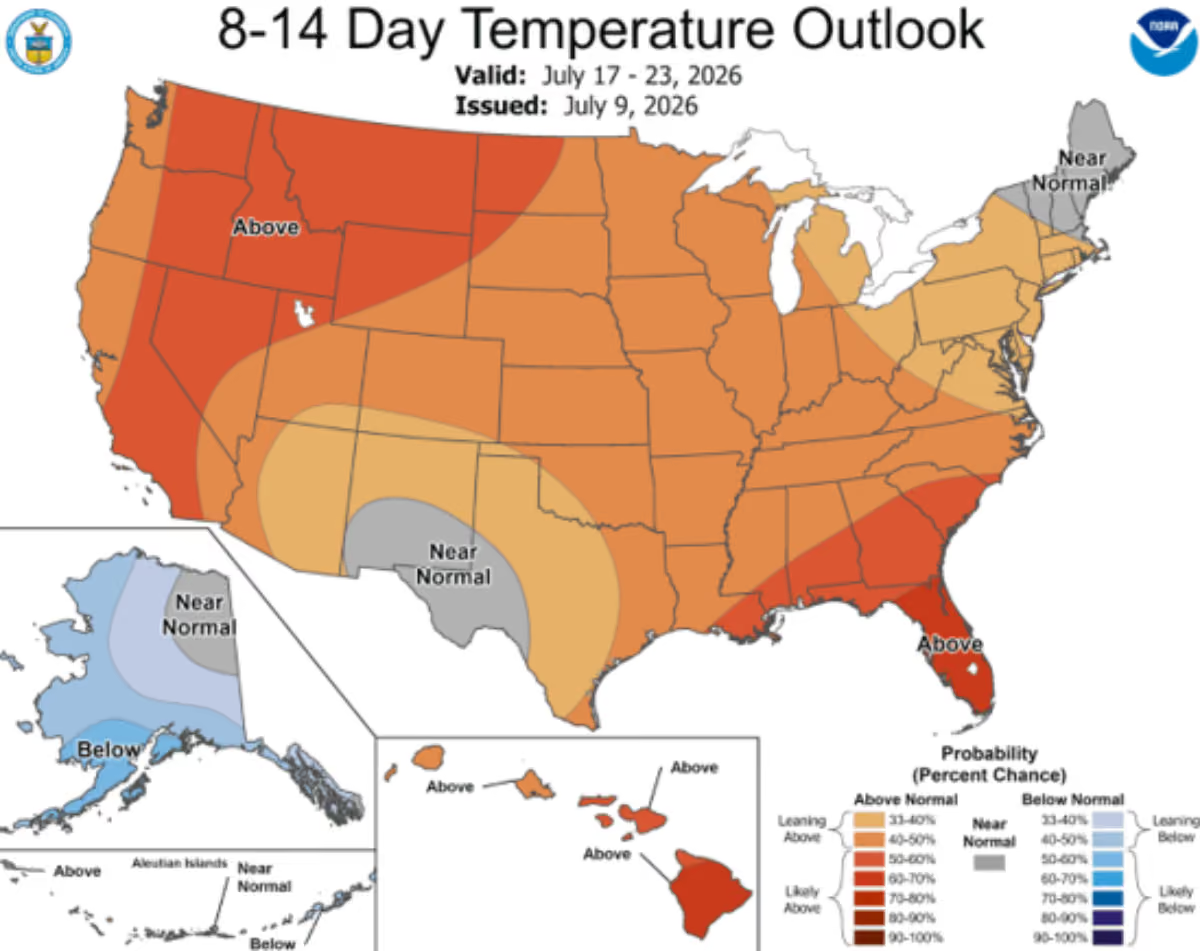

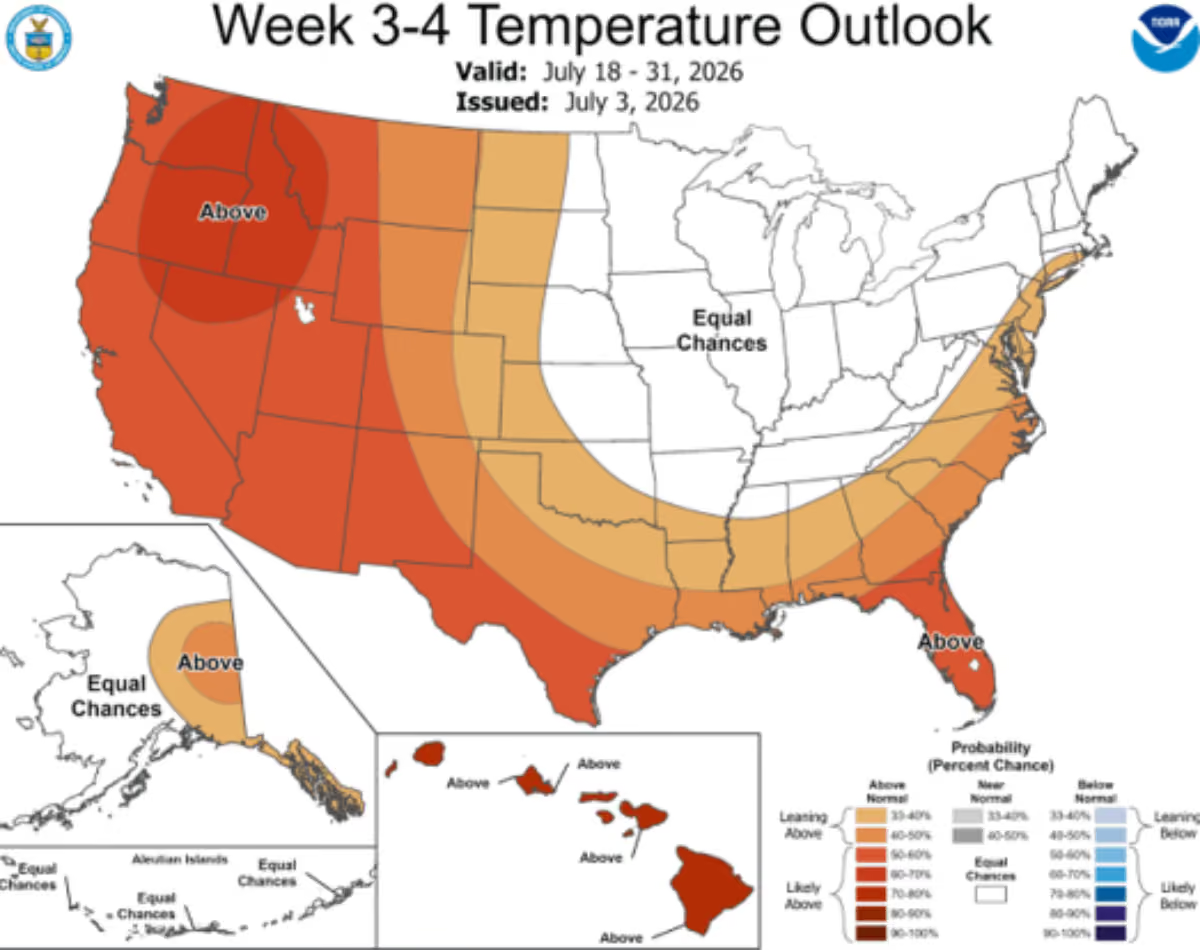

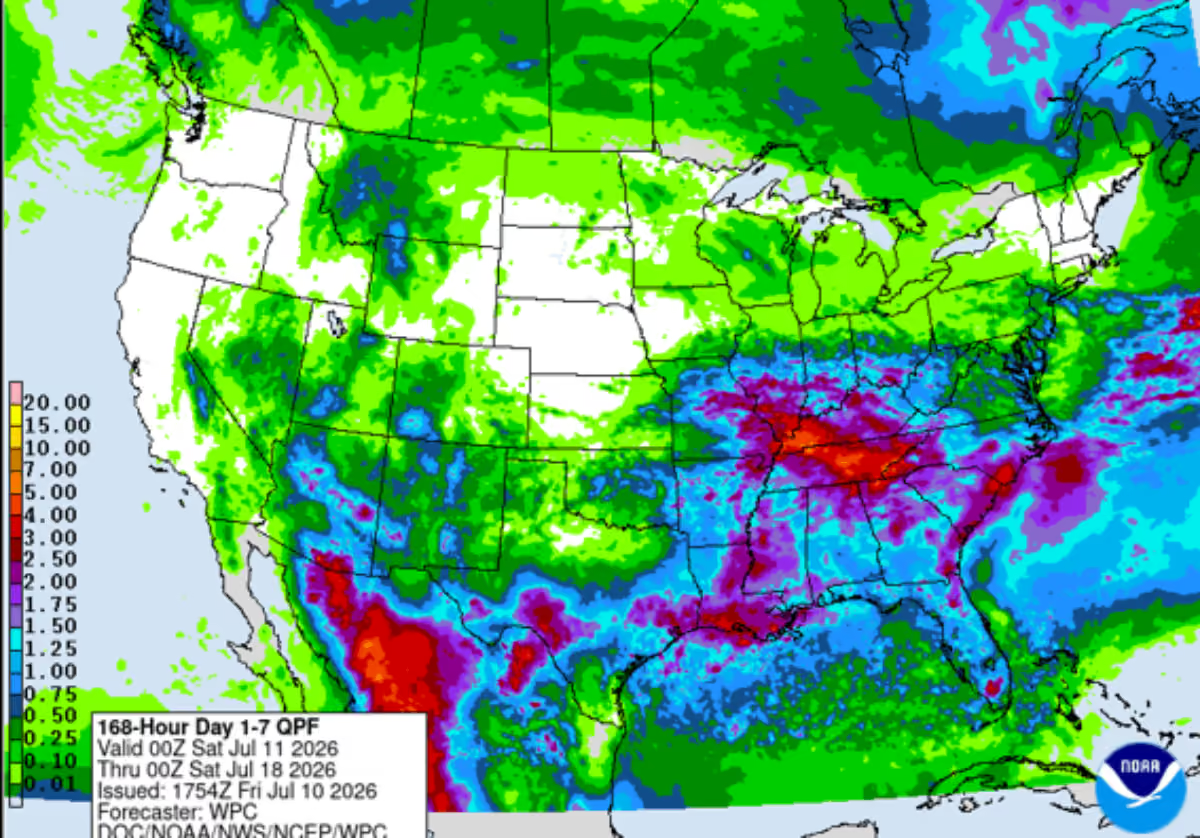

The near-term precipitation outlook shows potential heavy rains for Southeast Missouri and the lower Ohio River Valley, but dry in Arkansas and the upper Midwest. The 2-3 week forecast shows close to normal chances for precipitation. Temperatures are expected to be normal to above normal for the next 3-4 weeks.

NWS 7 day Precipitation Forecast

NOAA Precipitation and Temperature General Outlook