RF Insights: February Market Update

Grayson Daniels, VP of Grain Sales and Procurement, provides a Market Update for February.

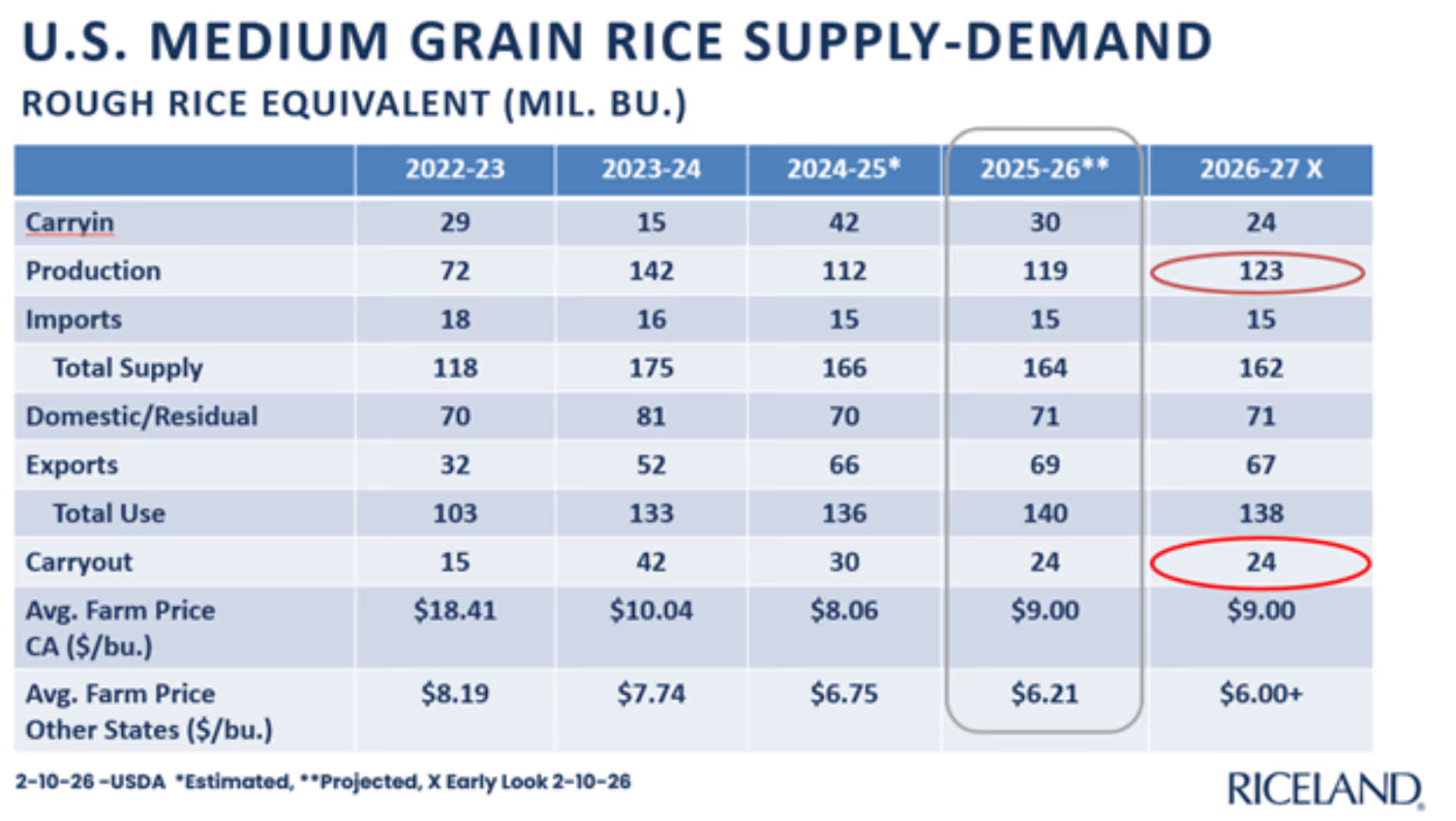

Rice Fundamental Highlights

- The February WASDE report reduced imports, which is positive, however, exports were reduced by a larger magnitude due to lagging rough rice exports.

- The net of these changes led USDA to increase old crop ending stocks from 77 million bushels to 81 million bushels.

- Export demand for rough rice has picked up, however the pace for the current year remains well behind year-ago levels.

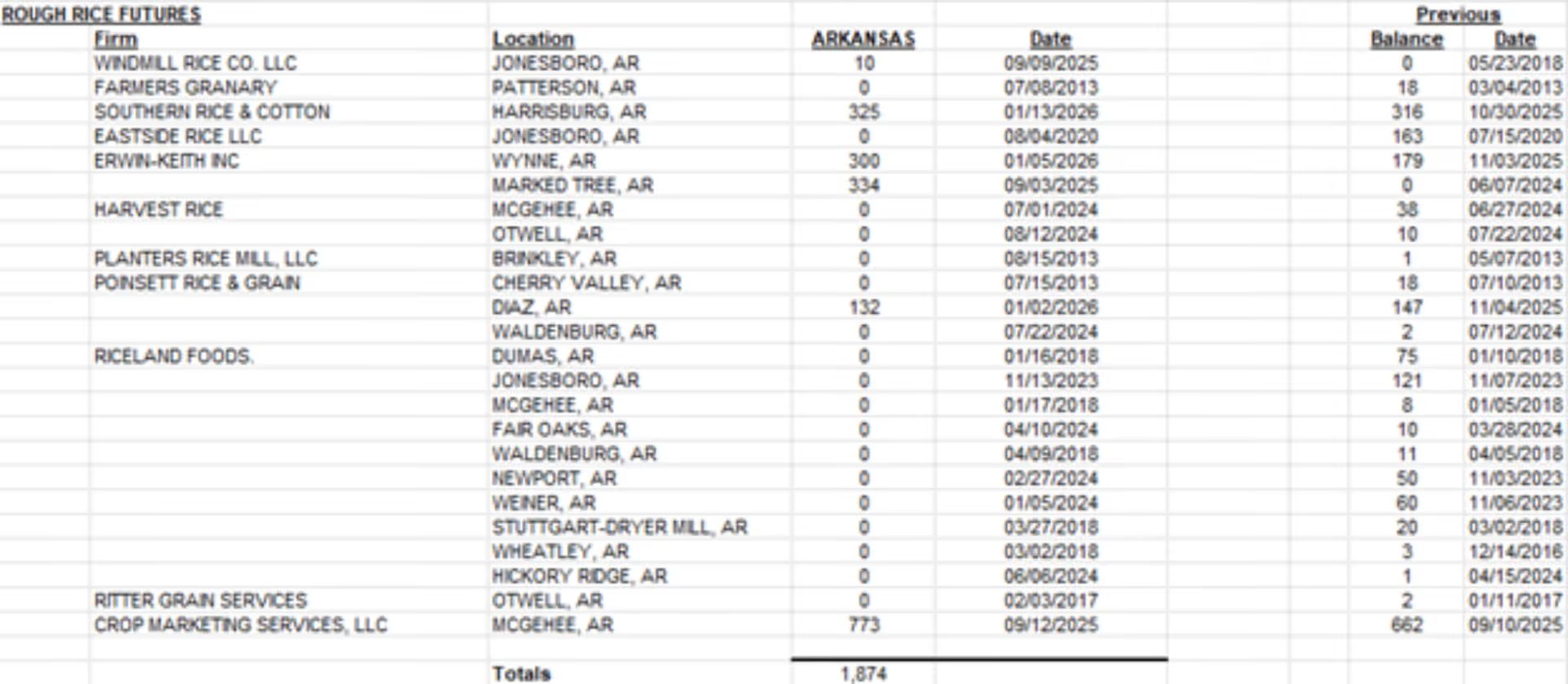

- CBOT receipts are unchanged from last month, at 1,874.

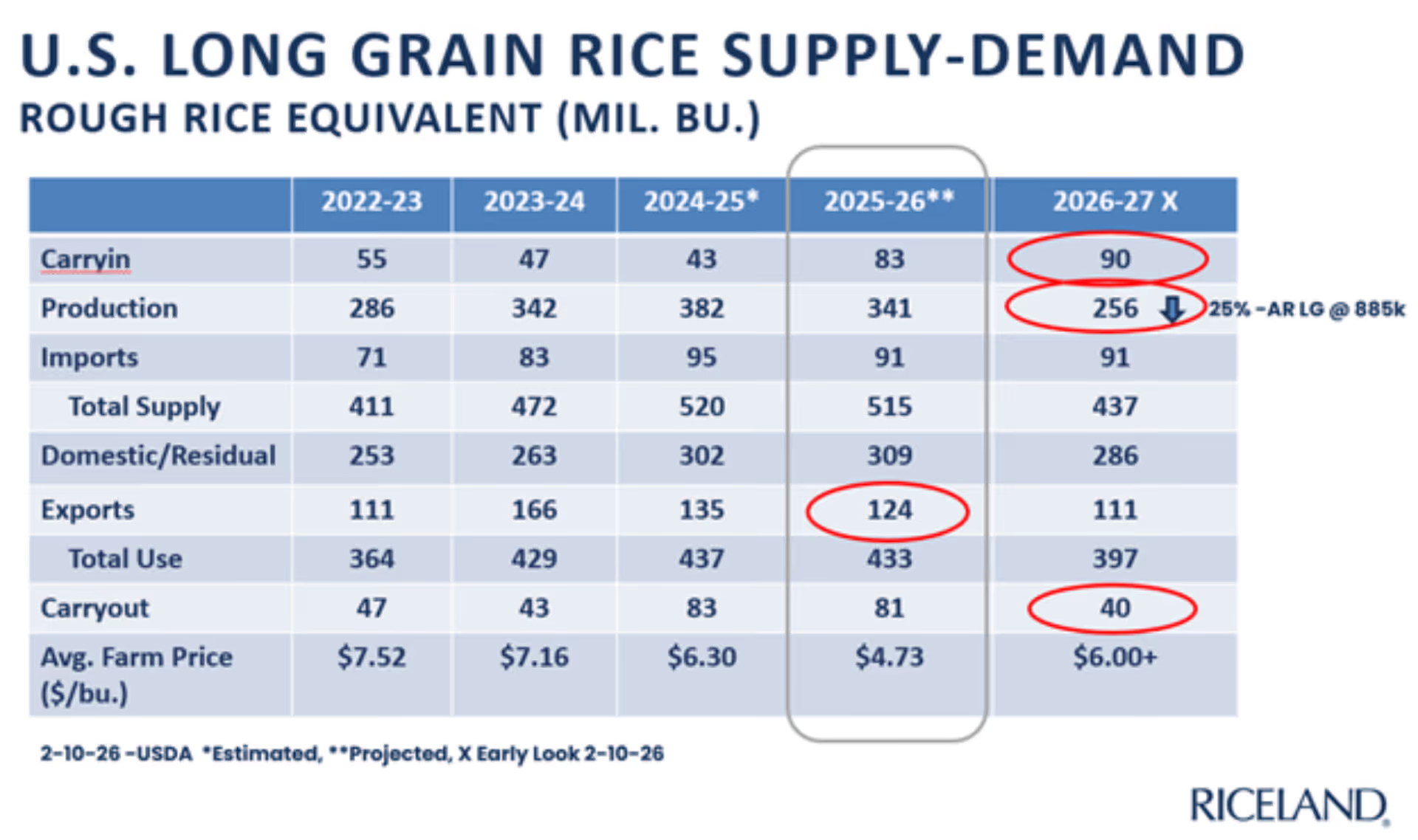

- Rice acres are widely expected to drop approximately 25% from last year.

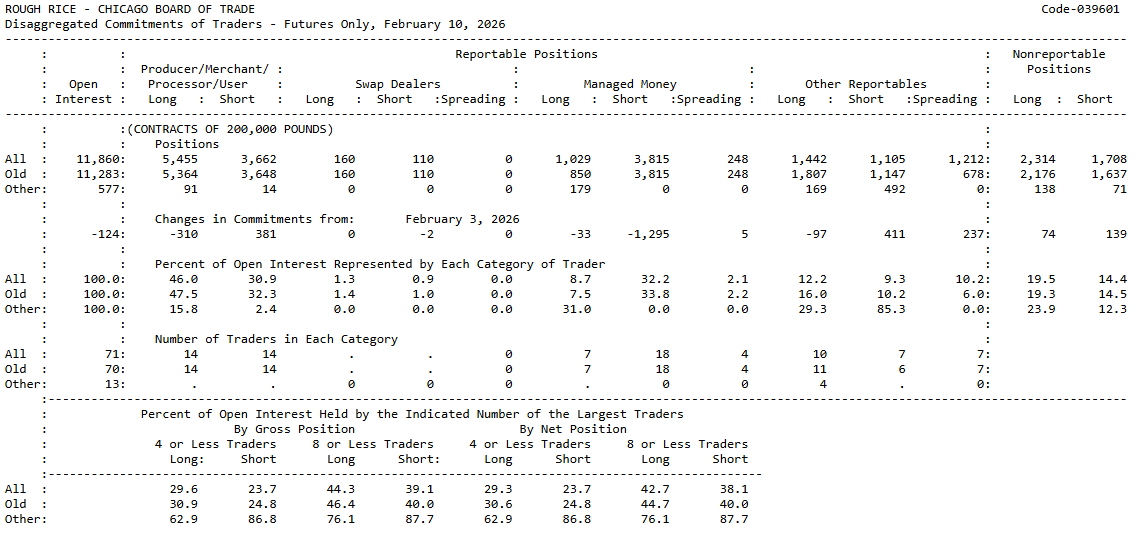

- CFTC Commitments of Traders still show the fund segment is net short approximately 2,800 contracts, sharply lower than the 7,000 net short a few months ago.

- Early look at the 2026 balance sheet shows long grain stocks could tighten dramatically into 2027 if acres are reduced 25%, even with beginning stocks higher than USDA’s current old crop ending stocks.

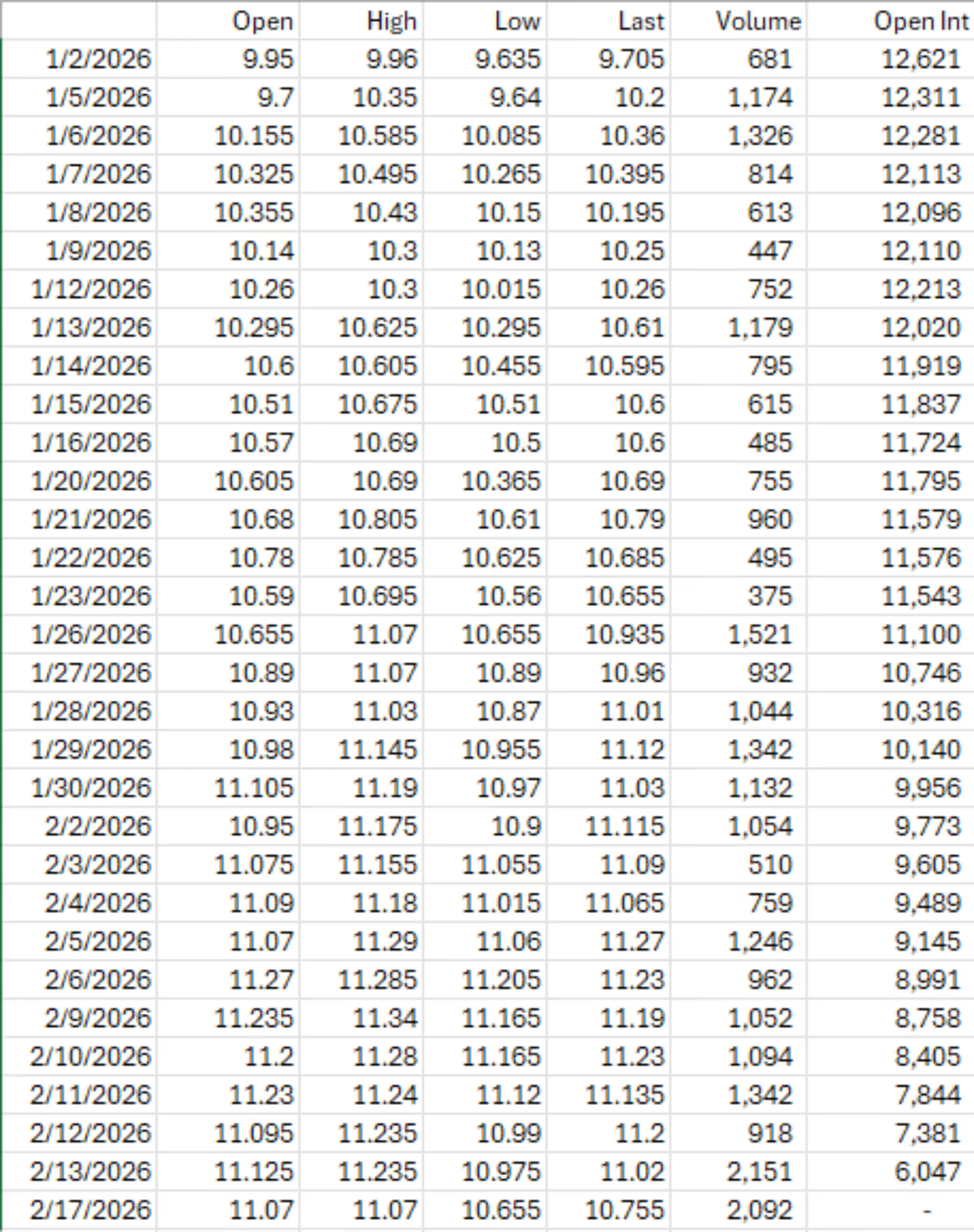

Old Crop Rough Rice Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

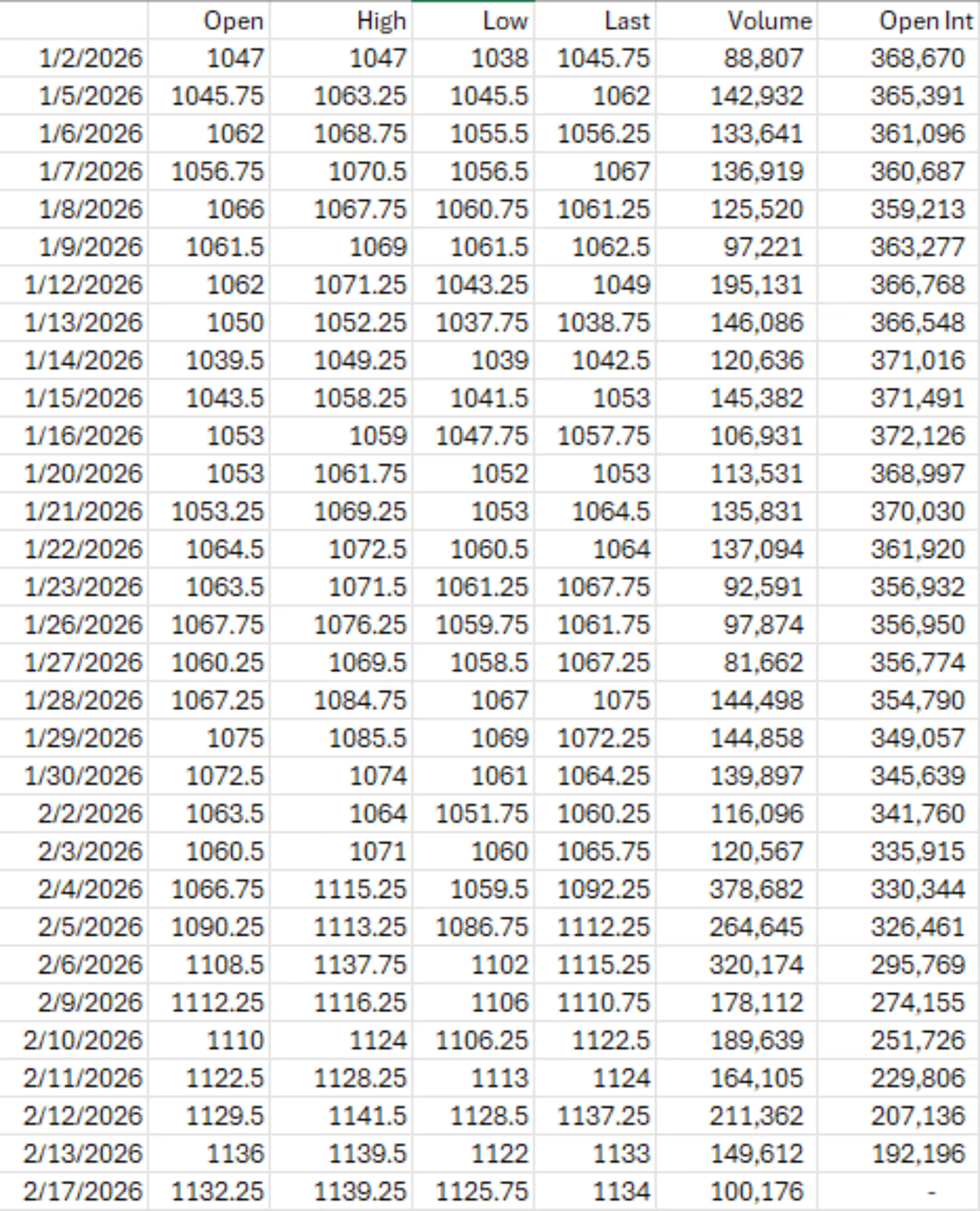

CBOT March ’26 Rough Rice Values, 1/2/26 through 2/17/26

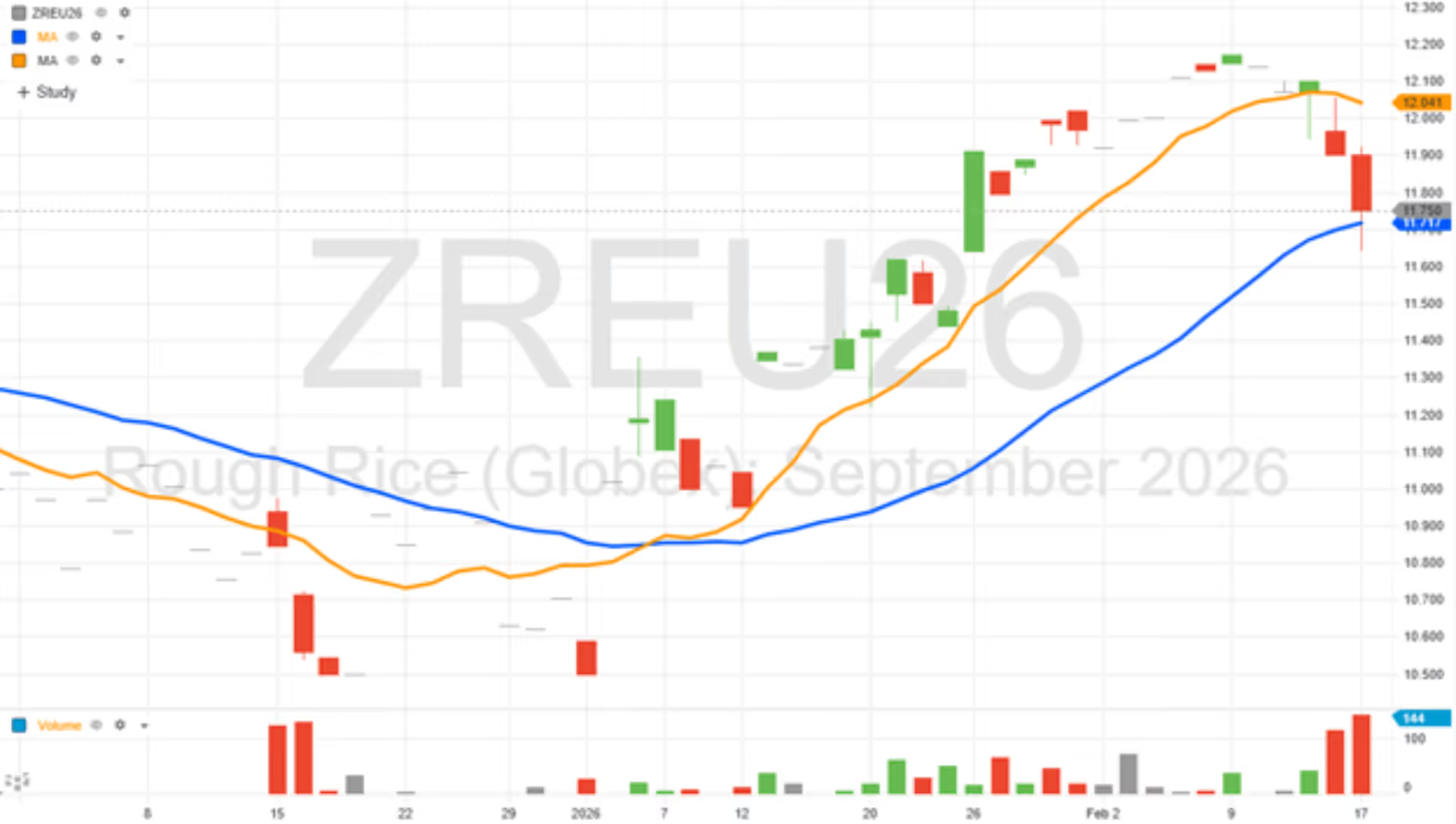

September ‘26 Rough Rice Futures

Orange Line = 9 day moving average

Blue Line = 27 day moving average

CBOT Receipts As of 2-12-26

CFTC Commitments of Traders

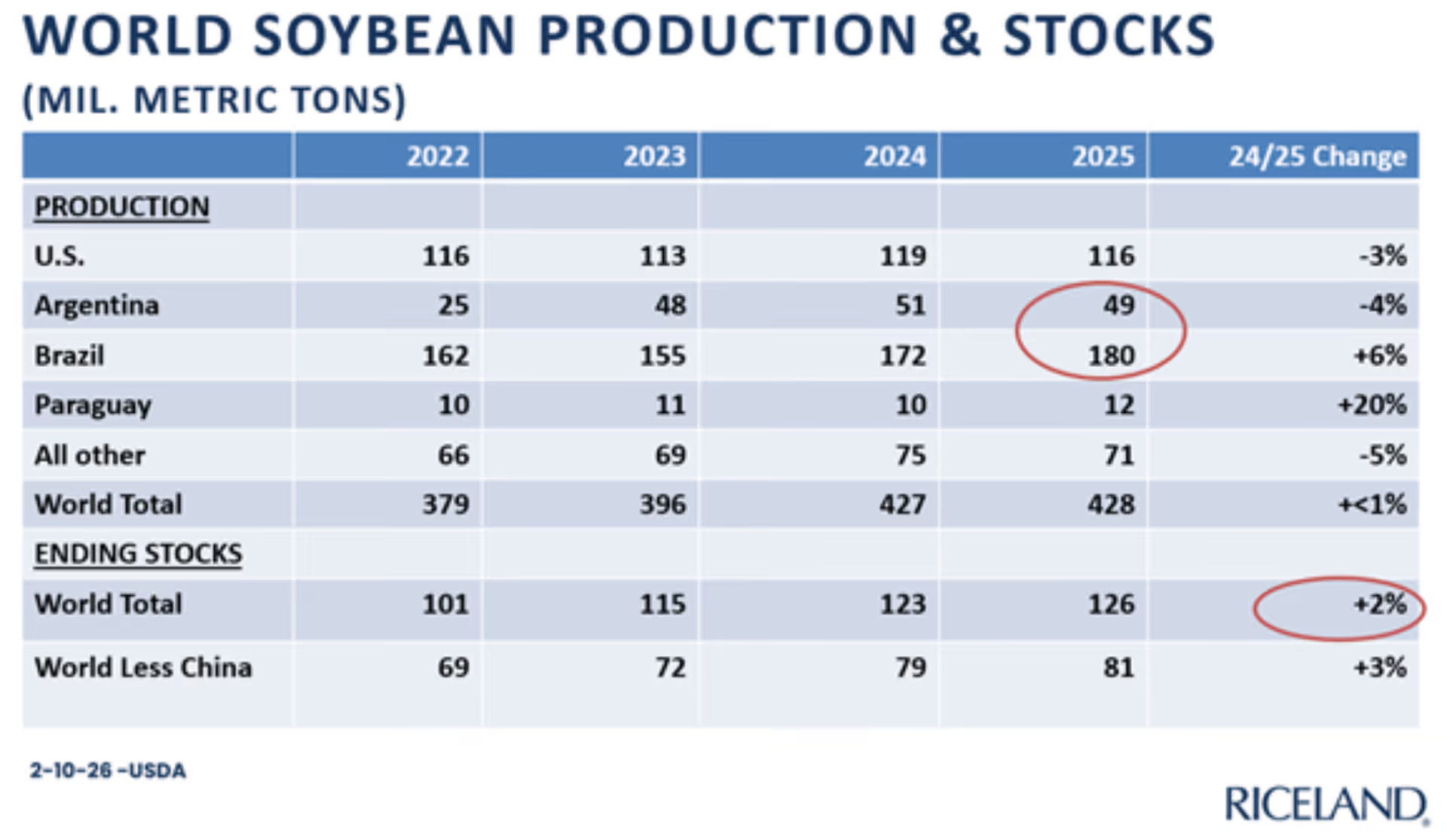

Soybean Fundamental Highlights

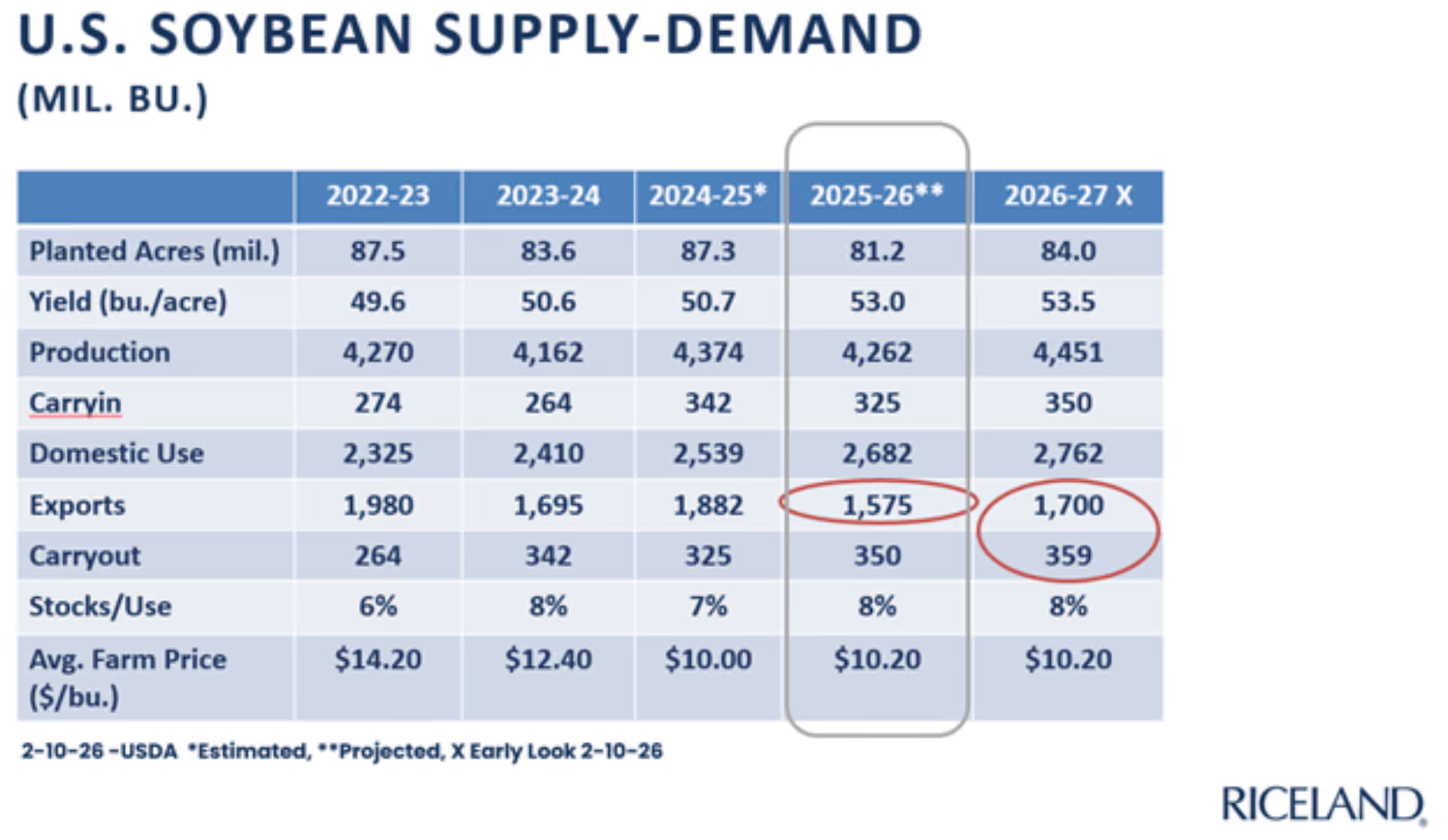

- The February WASDE made zero changes to the soybean balance sheet compared to the January report.

- Ending stocks are projected at 350 million bushels.

- The market has rallied in February on the potential for additional purchases from China, beyond the 12 million metric tons agreed to in October. U.S. prices are significantly higher than Brazil which could cause other countries to buy from Brazil, partially offsetting any increased China purchases.

- Traders also appear to be pricing in favorable RVO volumes from EPA, which could be official in March. The details of the 45Z biofuel tax credits were mostly as expected which was viewed as favorable to soybean demand.

- South American weather has been mostly favorable with a record crop expected in Brazil.

- U.S. planting intentions and EPA RVO volumes will be the key market drivers for the next several weeks.

- Early look at the 2026 balance sheet shows stocks could remain stable with U.S. acres at 84 million and exports increasing to 1.7 billion bushels.

Old Crop Soybean Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT March ’26 Soybean Values, 1/2/26 through 2/17/26

November ‘26 Soybean Futures

Orange Line = 9 day moving average

Blue Line = 27 day moving average

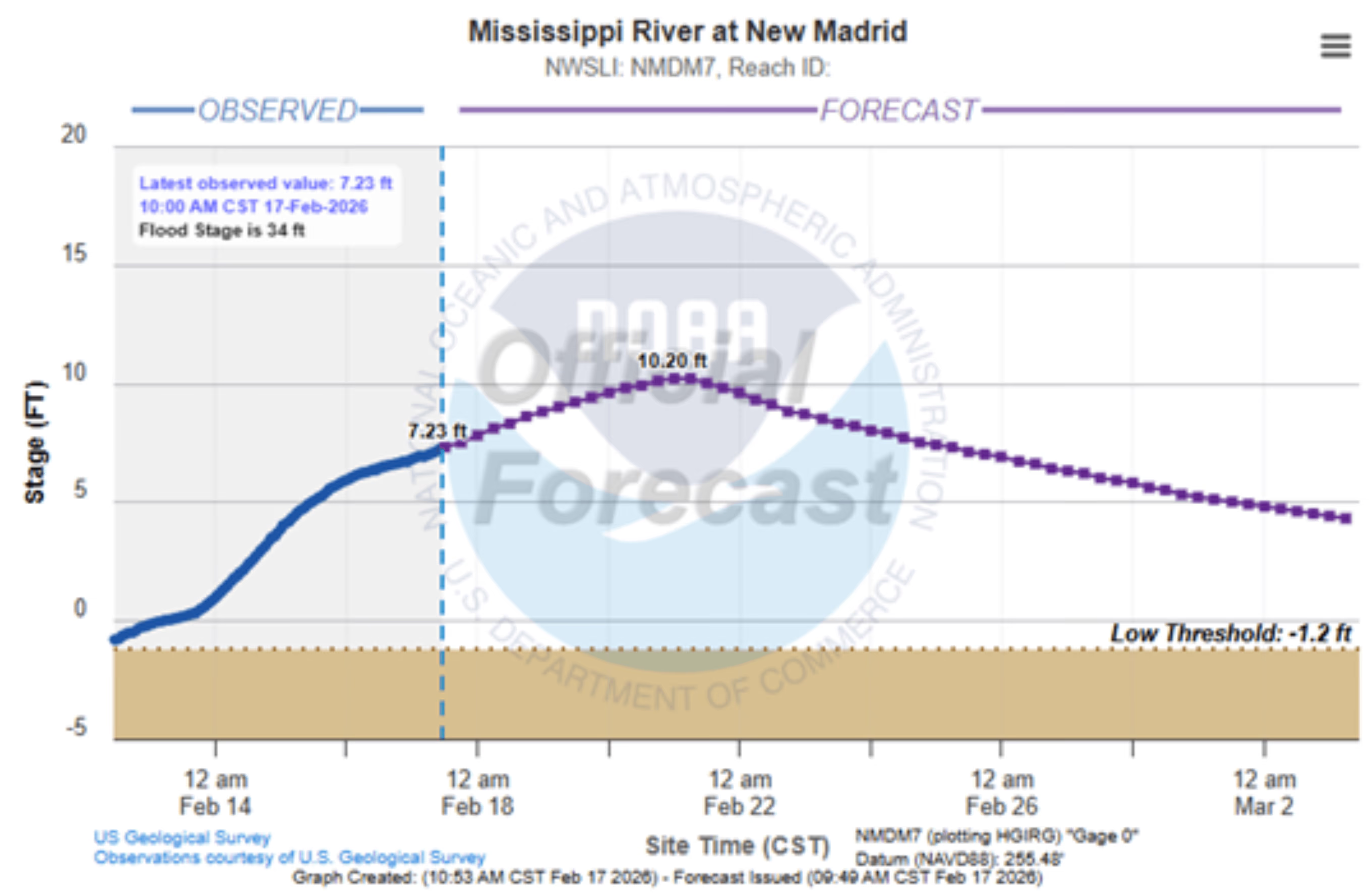

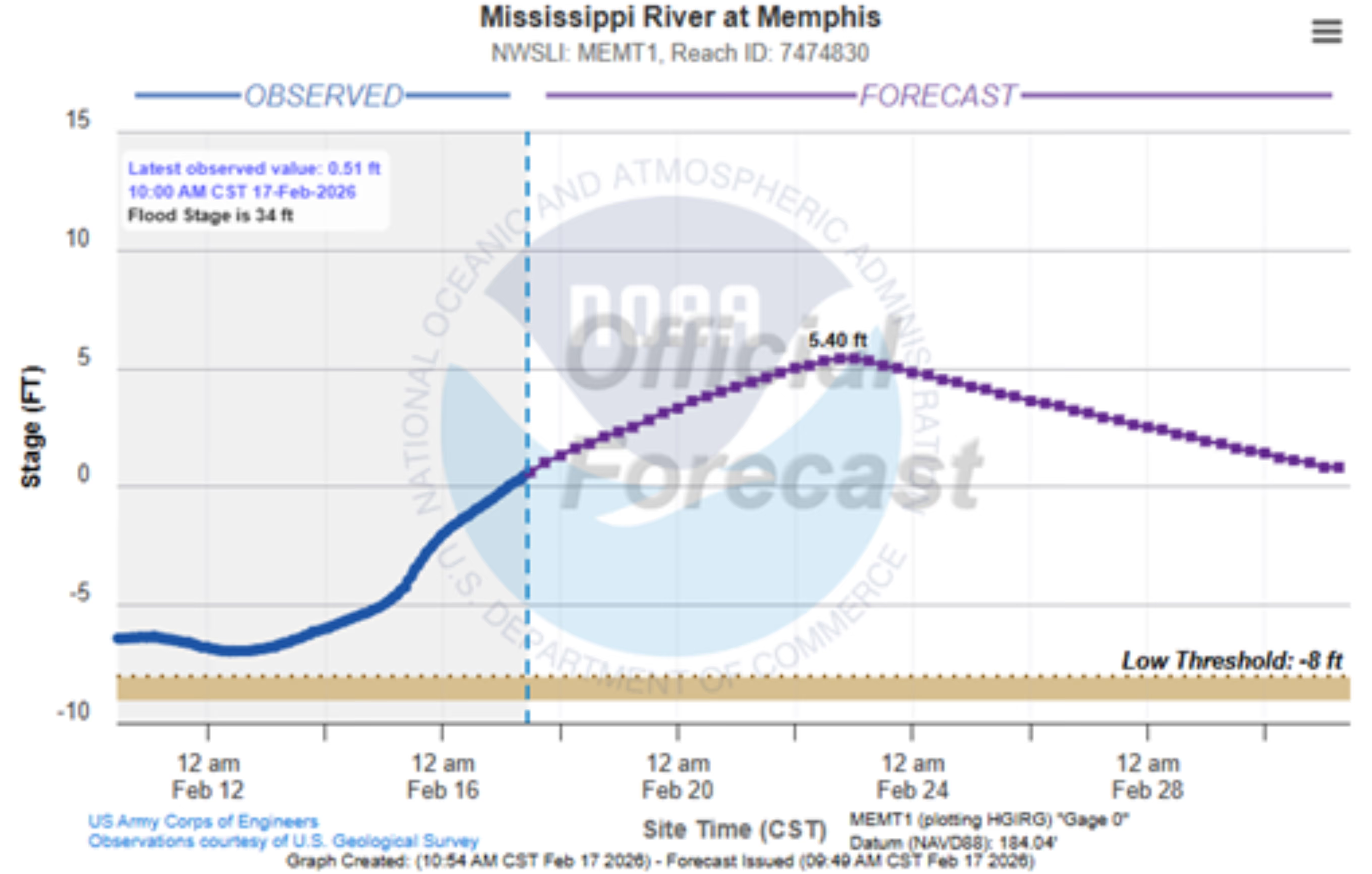

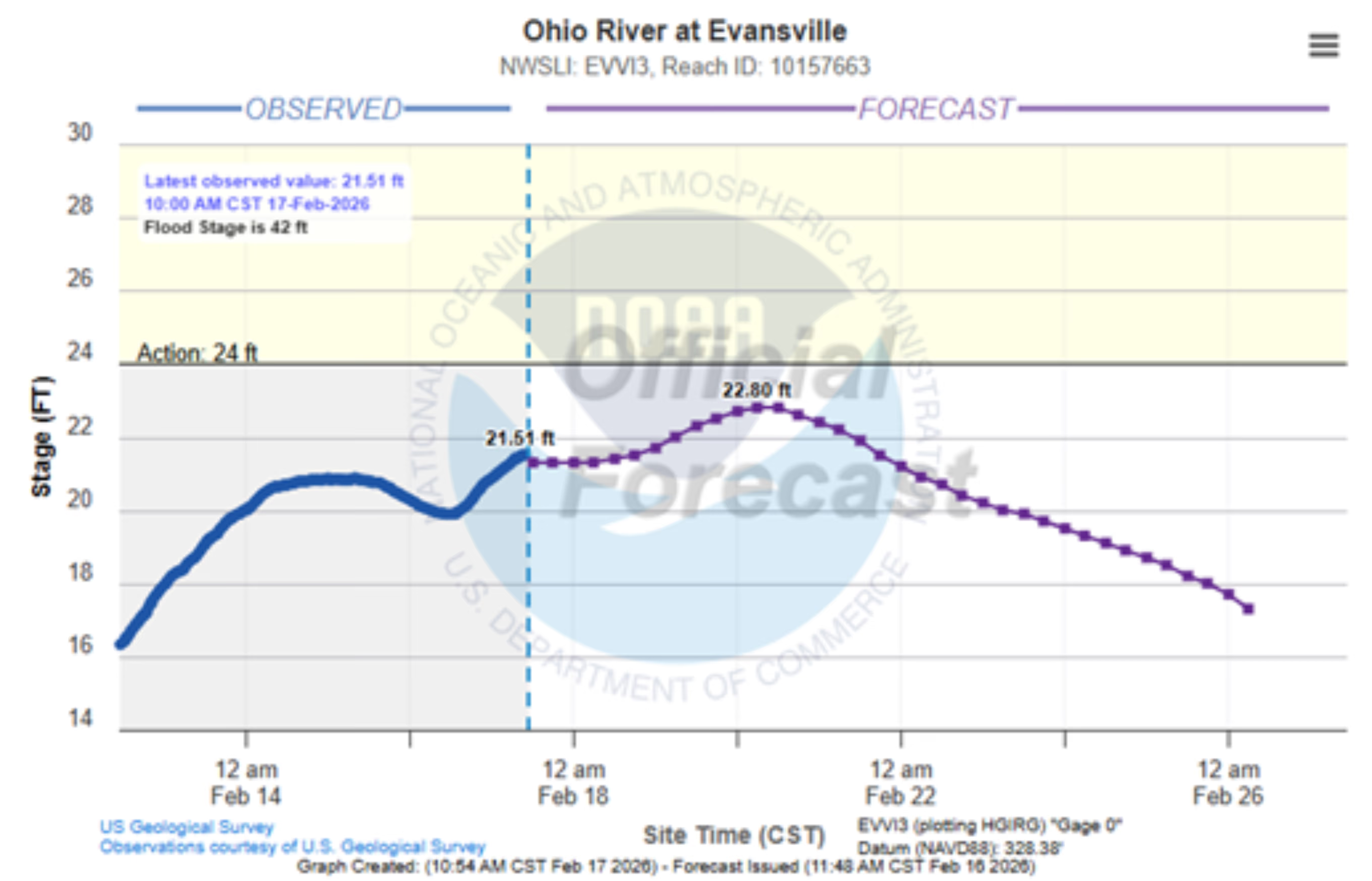

River / Weather

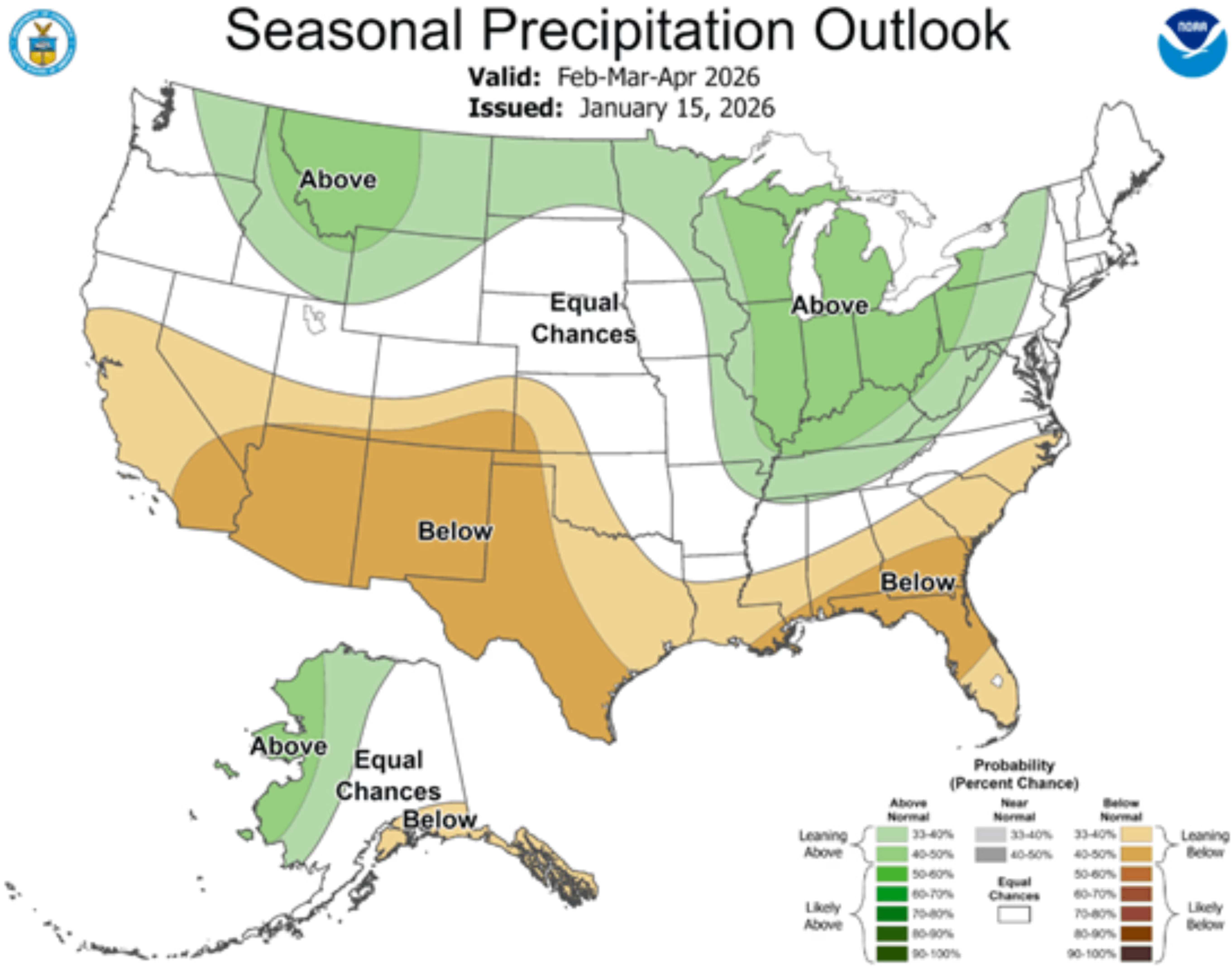

The Mississippi River graphs show ample water for navigation, albeit still low for this time of year. The Ohio River graphs show increased levels which should help as it flows South. The Ohio River Valley is forecast to receive above normal rainfall for the Spring.

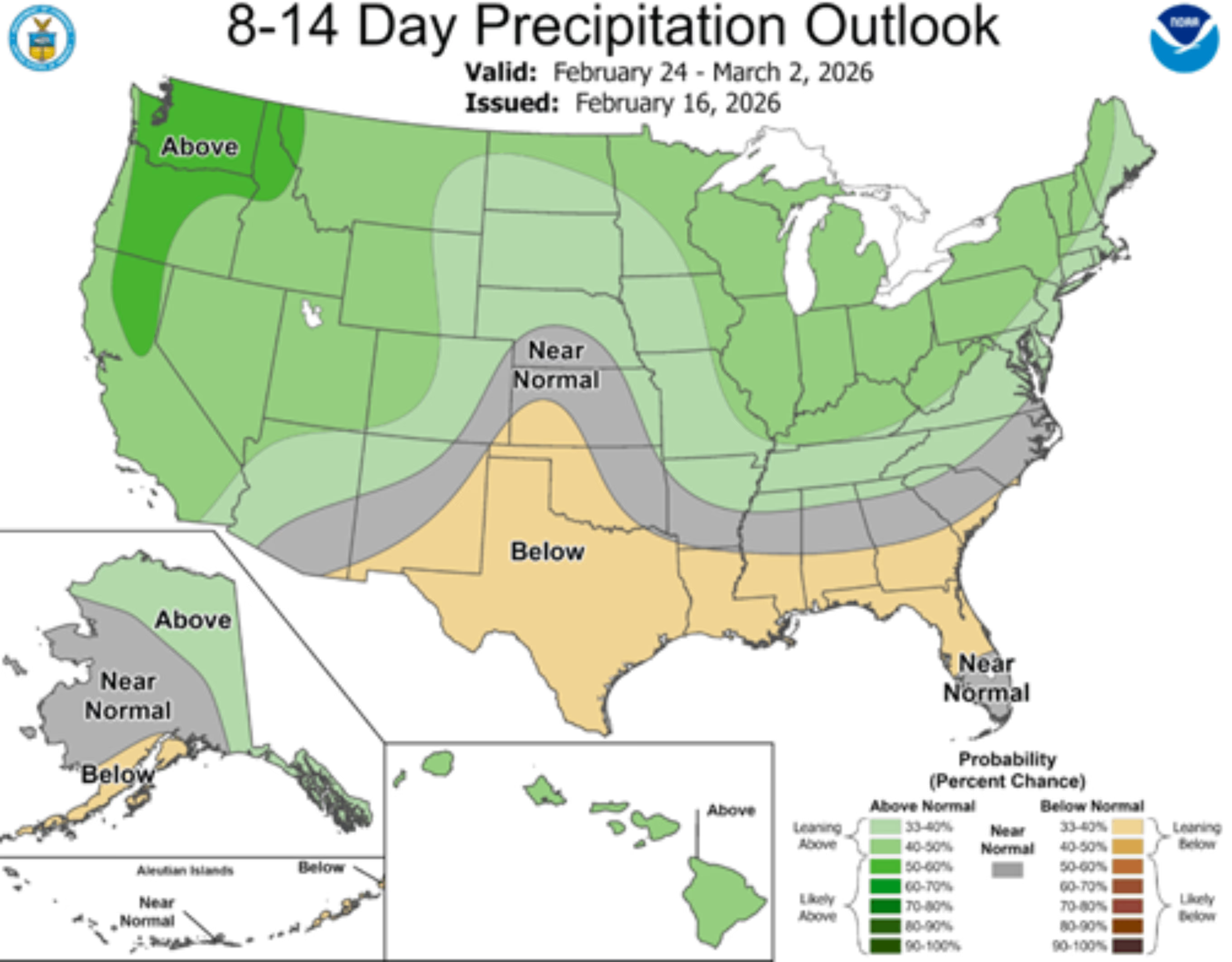

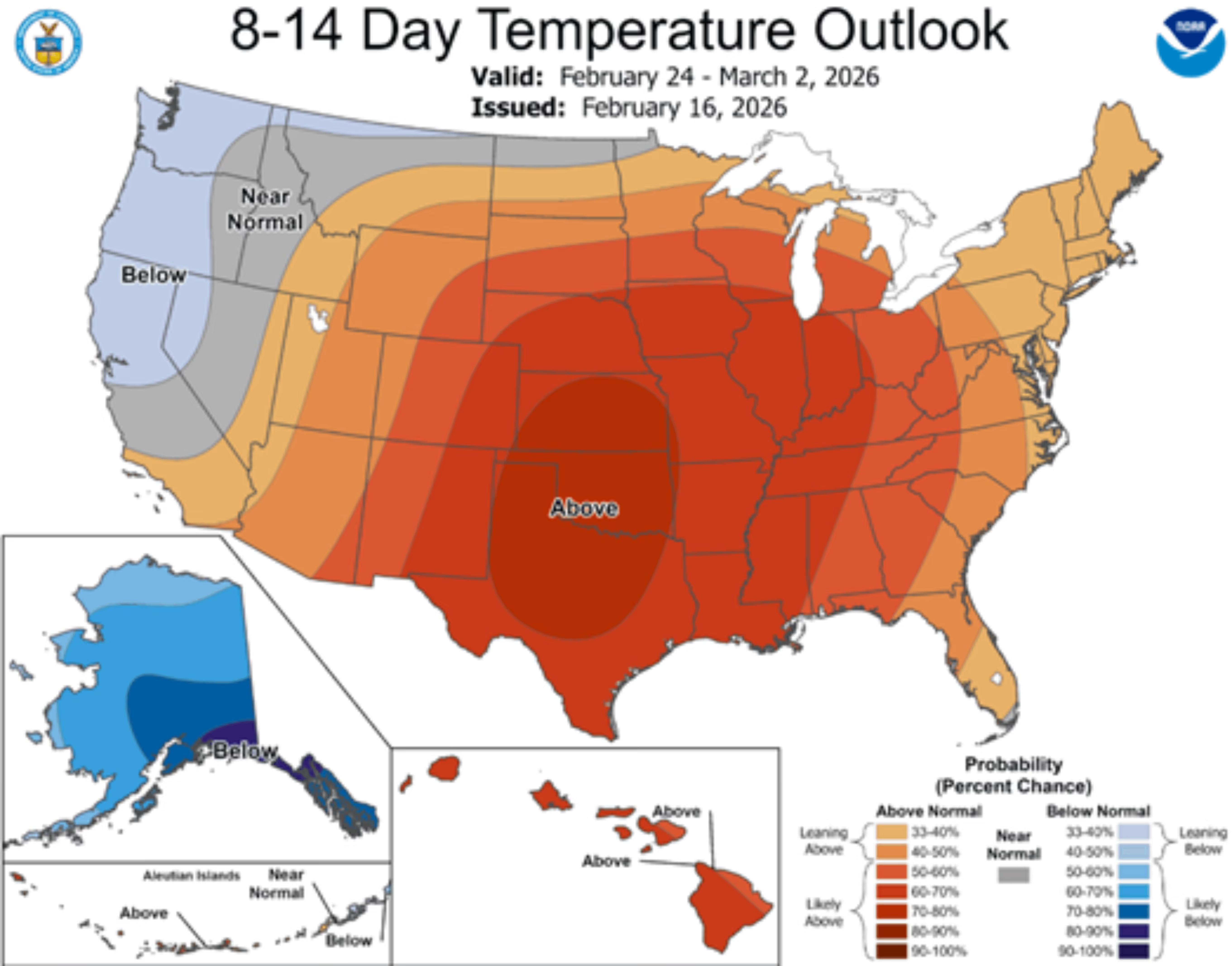

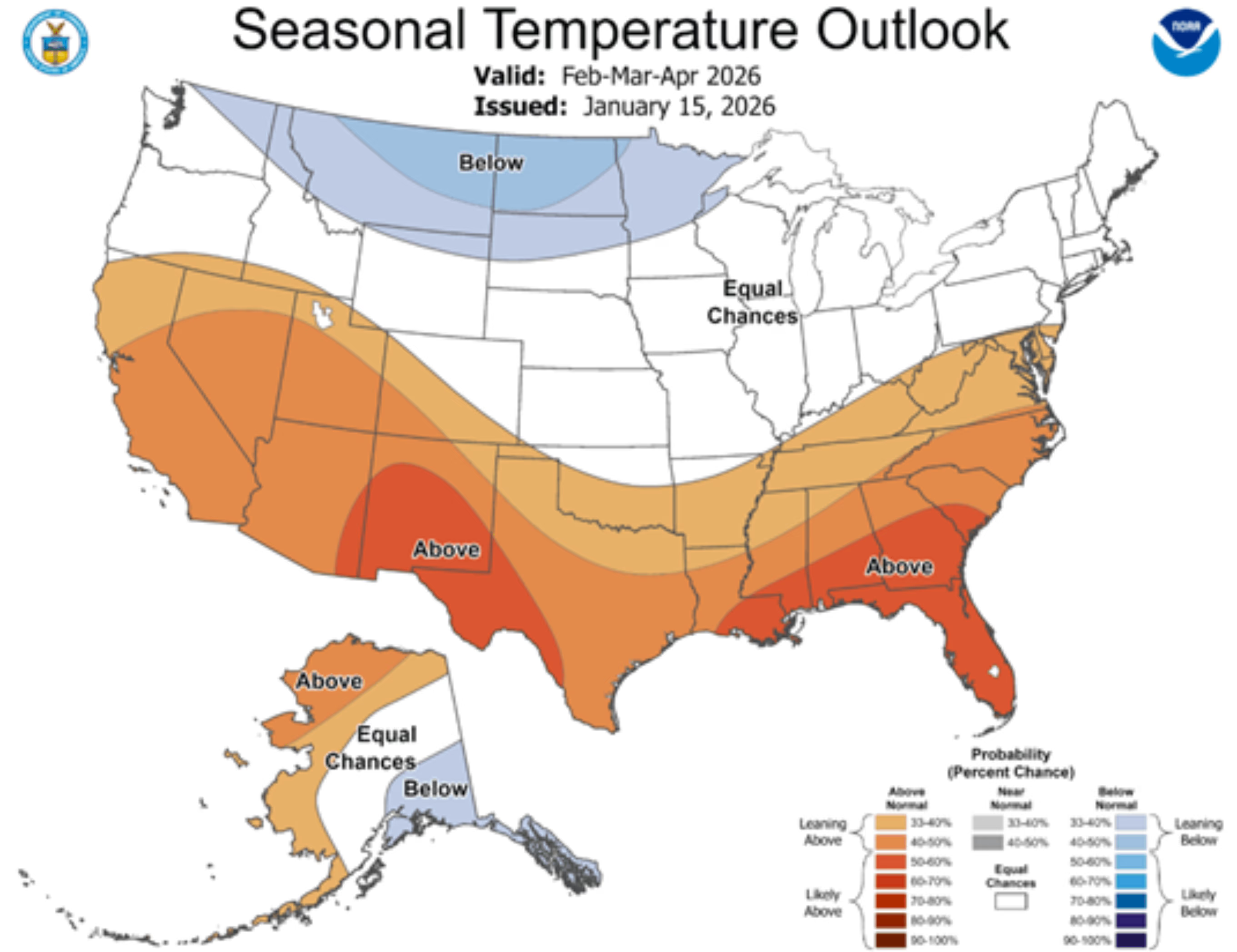

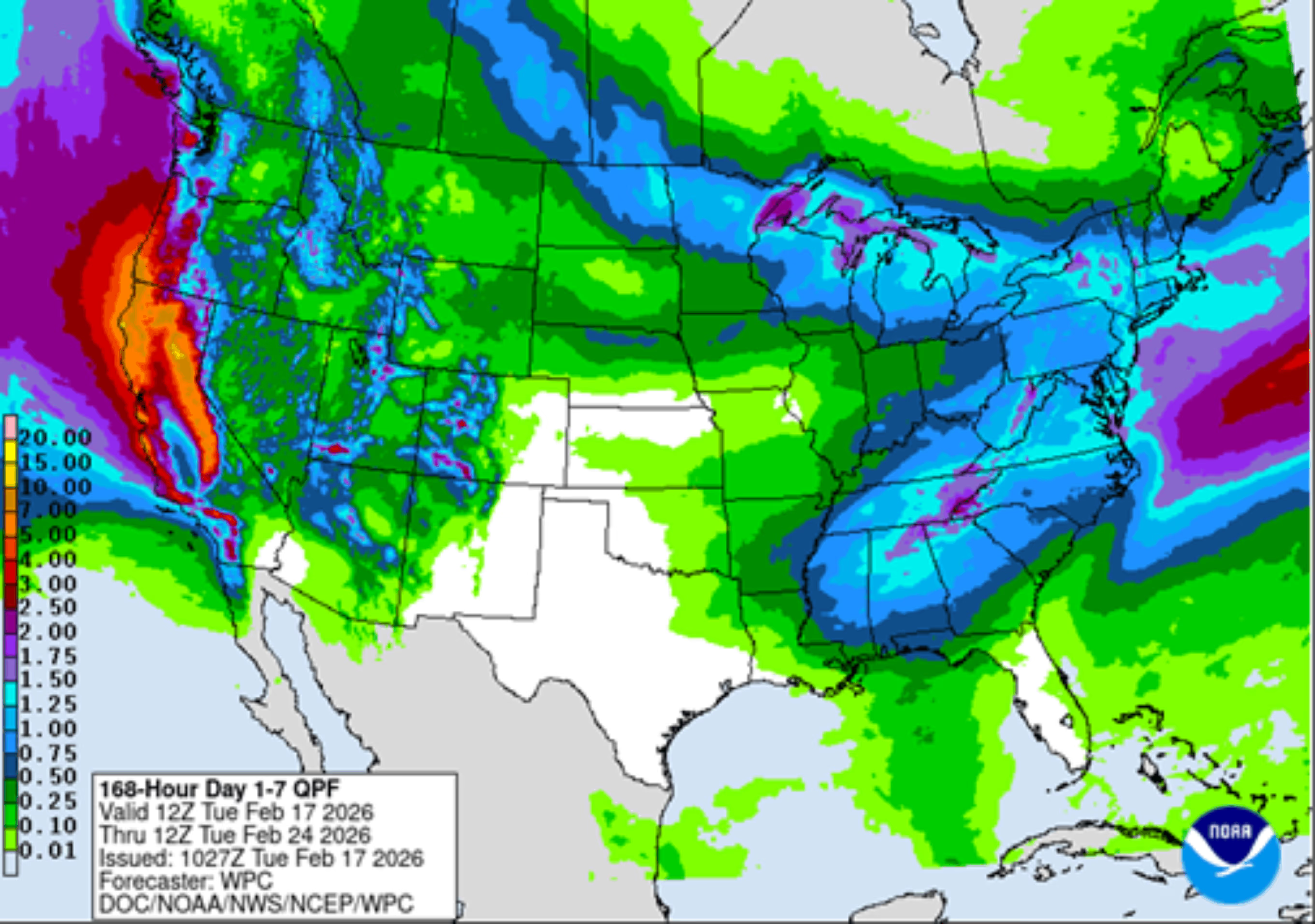

The near-term precipitation outlook shows some rain is possible for Eastern Arkansas and Southeastern Missouri. The long-term precipitation for the spring shows normal precipitation is expected. Temperatures are expected to be much above normal for the next couple weeks, with the long-term outlook also showing above normal temperatures for the spring.

NWS 7 day Precipitation Forecast

NOAA Precipitation and Temperature General Outlook