RF Insights: September Market Update

Grayson Daniels, VP of Grain Sales and Procurement, provides a Market Update for September.

Rice Fundamental Highlights

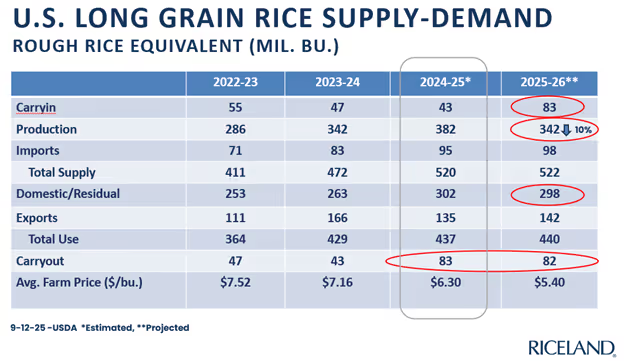

- USDA September 12 WASDE incorporated the August rice stocks resulting in old crop ending stocks decreasing from 88.4 mil. bu to 82.9 mil. bu, still the largest long grain stocks since 7/31/1986.

- For new crop the WASDE projected imports increasing to 98 million bushels despite the current tariff landscape.

- Yields were lowered for new crop but domestic use and exports were also reduced, resulting in ending stocks at 82.4 mil. bu, virtually unchanged from this year.

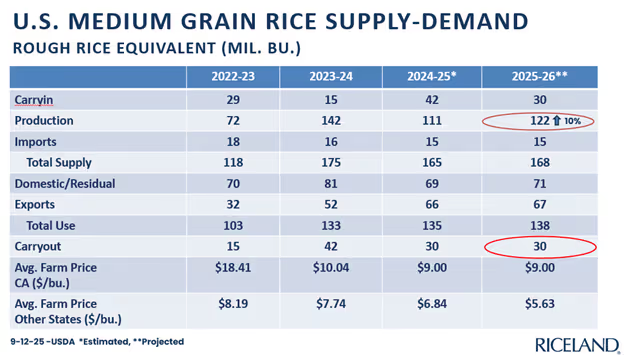

- Old crop medium grain stocks were revised upward 13 million bushels based on the August 1 stocks report.

- WASDE showed overall new crop medium grain production to be up 10% compared to 2024.

- Medium Grain ending stocks for 25/26 are projected at 30 mil. bu.

- Milled rice prices have stabilized after several weeks of decline.

- World rice stocks are projected to be ample, forecast at 187 million metric tons, down slightly from last year.

- Traders need to see new rice demand to spur higher futures values.

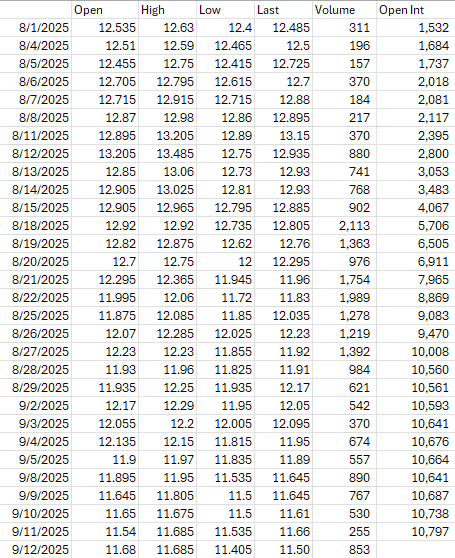

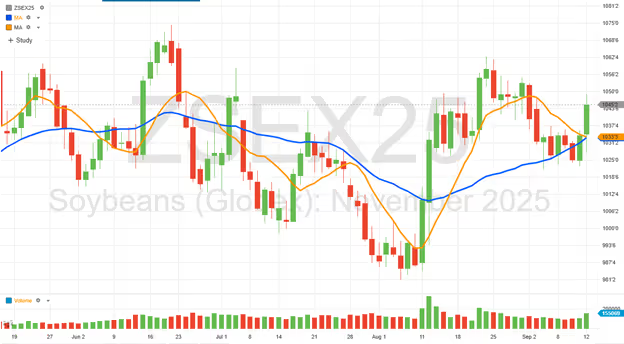

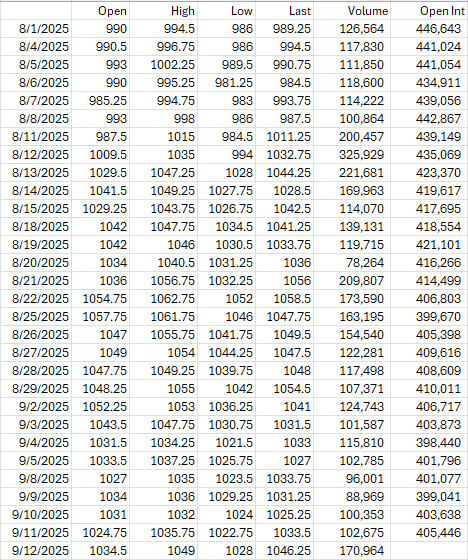

November ’25 Rough Rice Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT November ’25 Rough Rice Values, 8/1/25 through 9/12/25

U.S. Long Grain Rice Supply-Demand

U.S. Medium Grain Rice Supply-Demand

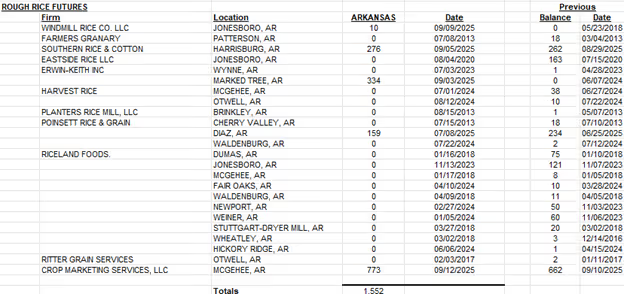

CBOT Receipts As of 9-12-25

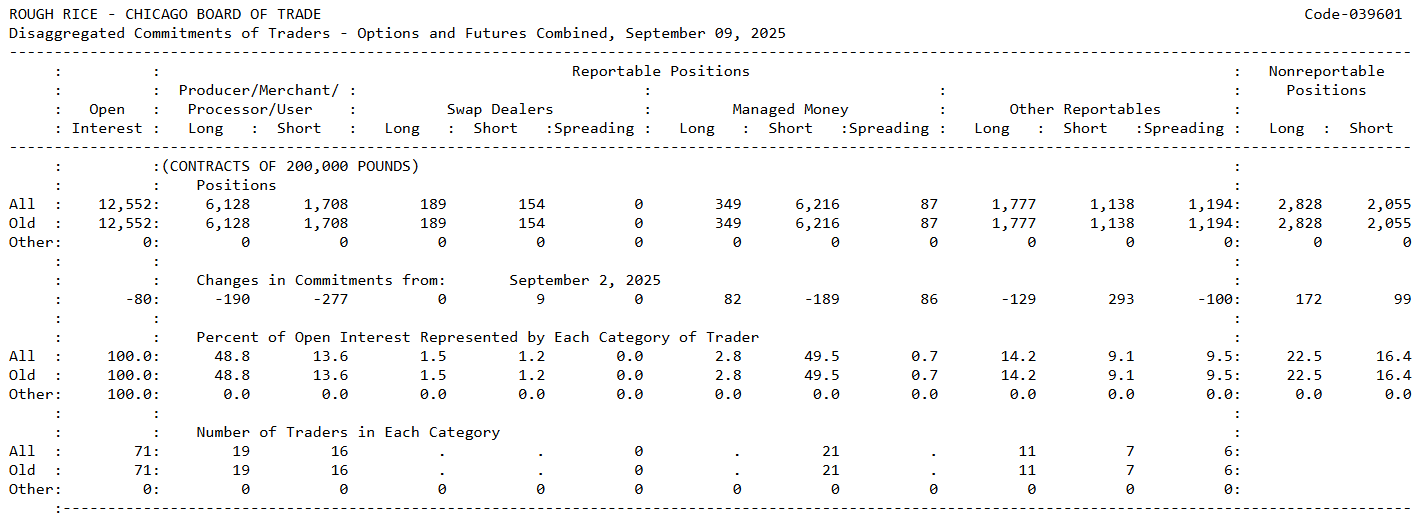

CTFC Commitment of Traders

Soybean Fundamental Highlights

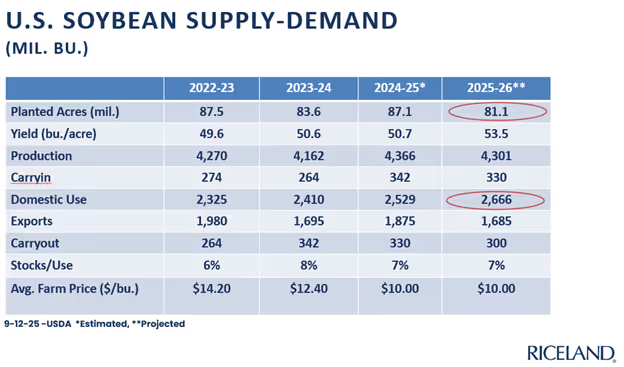

- The September 12 Supply and Demand report from USDA showed only slight changes to several data points. Planted area was revised upward slightly to 81.1 million acres and yield was revised down a tenth of a bushel to 53.5 bu. per acre.

- The projected ending stocks for new crop increased slightly to 300 mil. bu. after a slight decrease in exports and a slight increase in crush.

- The projected season average price for new crop was lowered to $10.00.

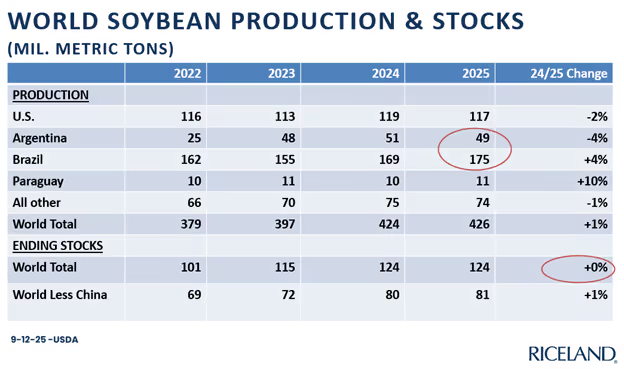

- World soybean stocks are projected to remain nearly flat after a few years of significant increases.

- Uncertainty regarding biofuel policy, remains a drag on the soybean complex. RVO proposed volumes from EPA were better than expected, but they won’t be finalized until later this year and there is lobbying to reduce the final volumes and reduce the penalties for imported biofuel feedstocks.

- Many traders believe USDA is still too high on exports given the absence of Chinese soybean purchases from the U.S.

November ’25 Soybeans

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT November ’25 Soybean Values, 8/1/25 through 9/12/25

U.S. Soybean Supply-Demand

World Soybean Production & Stocks

Weather Outlook

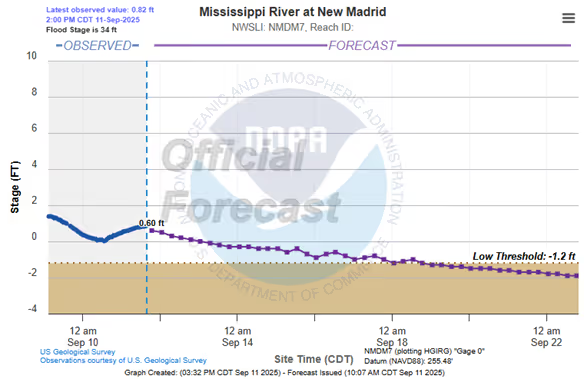

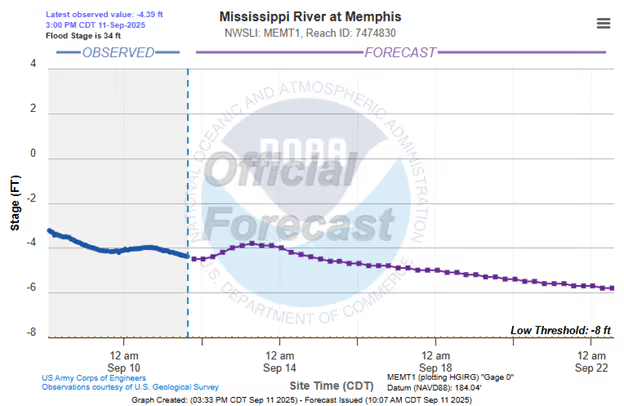

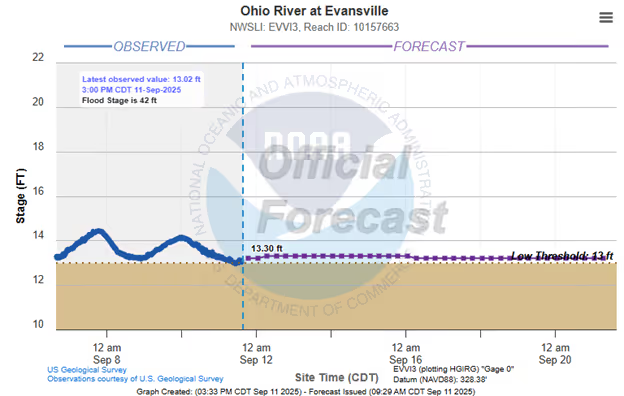

The Mississippi River and Ohio River graphs show declining levels during September. October could be problematic without rains in the upper Mississippi and Ohio River Valleys.

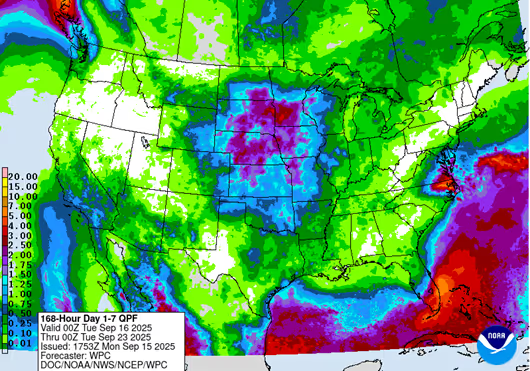

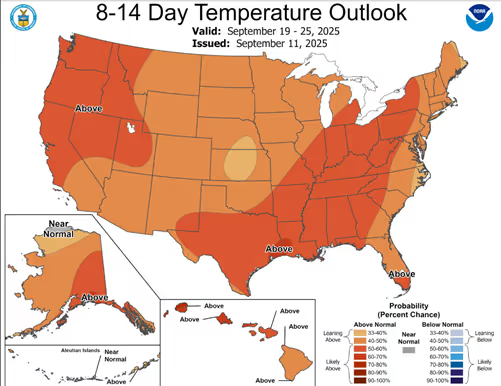

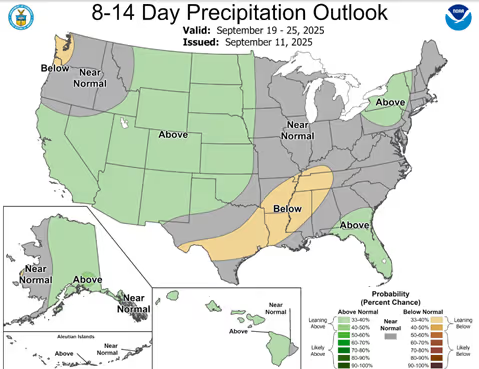

The near-term precipitation outlook shows no significant rain likely for Eastern Arkansas. Temperatures are expected to be above normal for the next few weeks.

NOAA Temperature General Outlook

NOAA Precipitation General Outlook

NWS 7-Day Precipitation Outlook