RF Insights: August Market Update

Grayson Daniels, VP of Grain Sales and Procurement, provides a Market Update for August.

Rice Fundamental Highlights

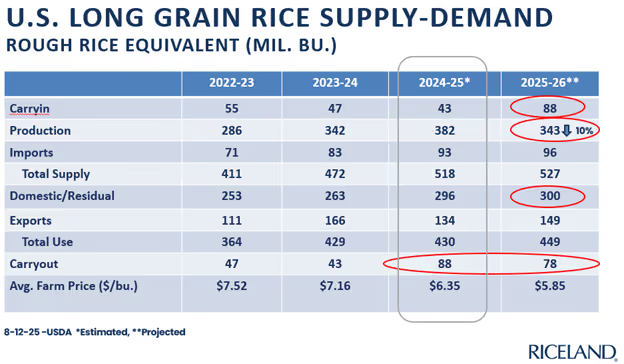

- USDA August 12 WASDE incorporated the August FSA certified acres which shocked most market participants with a higher than expected Arkansas and Missouri long grain acreage number, 1,172,000 and 211,000 respectively.

- USDA increased old crop carryout to 88.4 million bushels, the largest long grain stocks since 7/31/1986.

- For new crop the WASDE projected imports at 96 million bushels compared to 93 million bushels the previous year. After increasing domestic use and exports from the previous forecast, the projected long grain ending stocks increased to 78 million bushels. While this is down from the massive carryout this year, it still is much higher than needed to spark a sustained uptrend in the market.

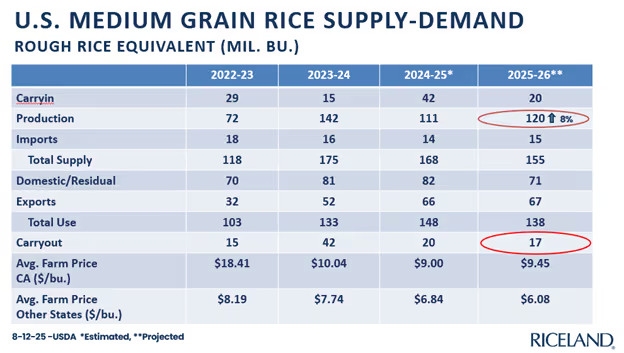

- WASDE showed overall Medium Grain production to be up 8% compared to 2024.

- Medium Grain ending stocks for 25/26 are projected at 17 mil. bu., down 3 million bushels from the previous year.

- Long grain rough rice exports continue to be poor.

- Milled rice prices have been declining.

- World rice stocks are projected to be ample, forecast at 187 million metric tons, nearly the same as last year.

September ’25 Rough Rice Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT September ’25 Rough Rice Values, 7/1/25 through 8/13/25

U.S. Long Grain Rice Supply-Demand

U.S. Medium Grain Rice Supply-Demand

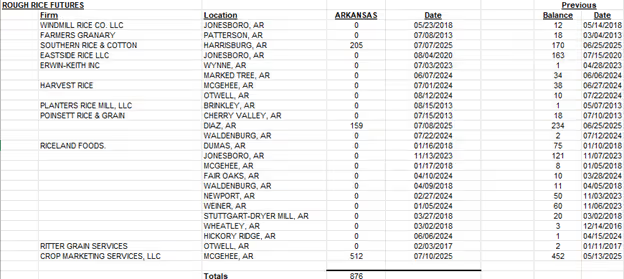

CBOT Receipts As of 8-11-25

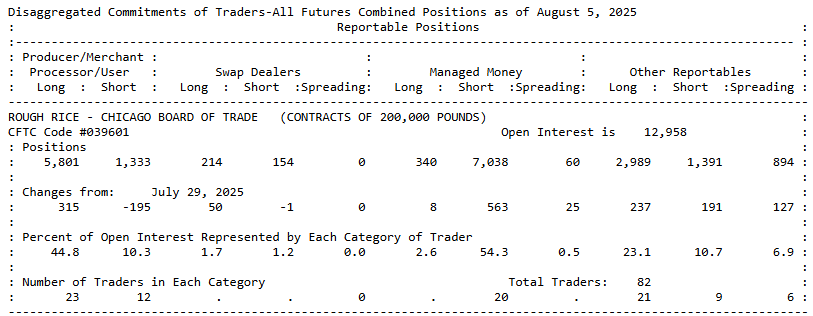

CTFC Commitment of Traders

Rice Market Summary

September futures were finally making a nice rally until the USDA numbers showed larger stocks and larger acres than expected. Fund traders have continued to maintain a very large short position. Farmer selling is very light given the low prices and given that we are very early in the marketing year. How the futures roll from Sep to Nov plays out and any new developments in demand will be key market inputs for the next several weeks.

Soybean Fundamental Highlights

- The August 12 Supply and Demand report from USDA shocked the market by reducing soybean acres by 2.5 million and increasing corn acres by 2 million.

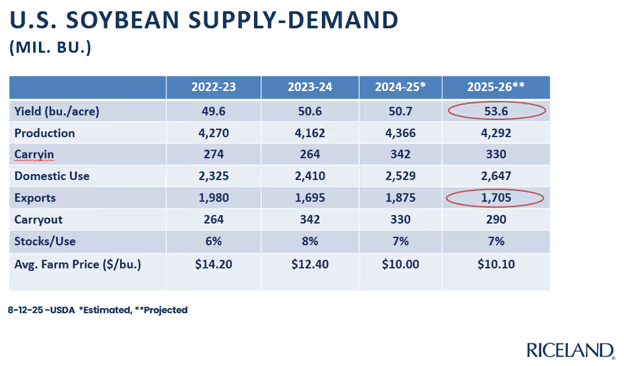

- Oldcrop ending stocks were reduced to 330 mil. bu.The projected average price for old crop was left unchanged at $10.00.

- The projected ending stocks for new crop dropped to 290 mil. bu. but this is dependent on 1.7 billion bushels of exports, which may be difficult to achieve.

- The projected season average price for new crop was left at $10.10.

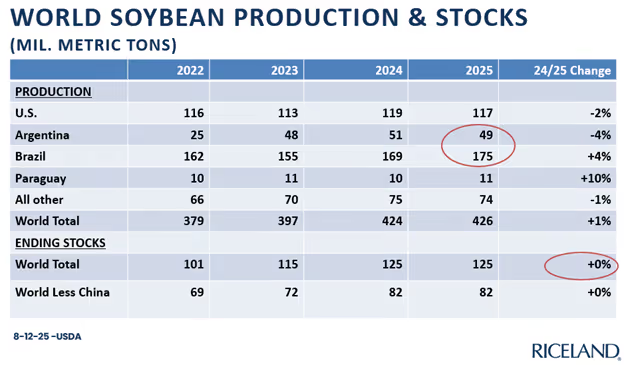

- World soybean stocks are projected to remain nearly flat after a few years of significant increases.

- There is still too much uncertainty regarding biofuel policy. RVO volumes won’t be finalized for several months, 45Z tax implications are uncertain, and SRE (Small Refinery Exemptions) volumes are uncertain and will have a major bearing on biofuel volumes.

November ’25 Soybeans

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT November ’25 Soybean Values, 7/1/25 through 8/13/25

U.S. Soybean Supply-Demand

World Soybean Production & Stocks

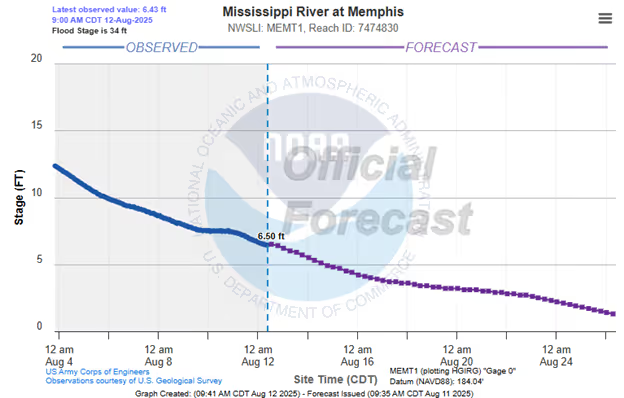

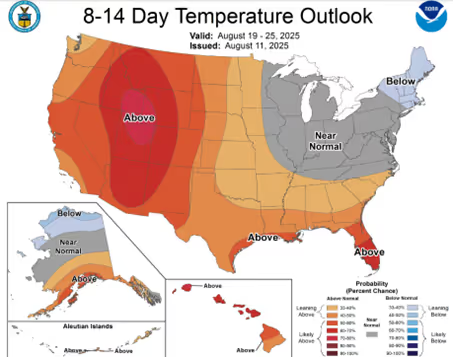

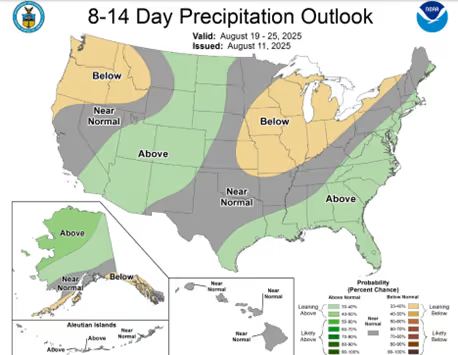

Weather Outlook

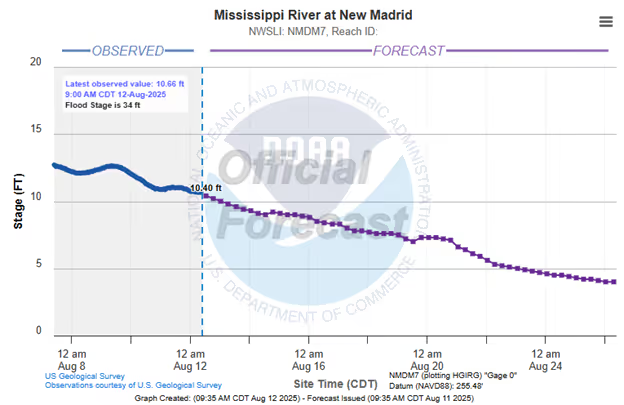

The Mississippi River and Ohio River graphs show declining levels during August. Late September and October could be problematic without rains in the upper Mississippi and Ohio River Valleys.

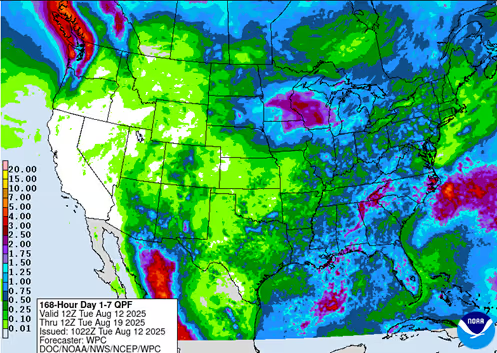

The near-term precipitation outlook shows only light rain likely for Eastern Arkansas. Temperatures are expected to be above normal for the next few weeks.

NOAA Temperature General Outlook

NOAA Precipitation General Outlook

NWS 7-Day Precipitation Outlook