RF Insights: June Market Update

Grayson Daniels, VP of Grain Sales and Procurement, provides a Market Update for June.

Rice Fundamental Highlights

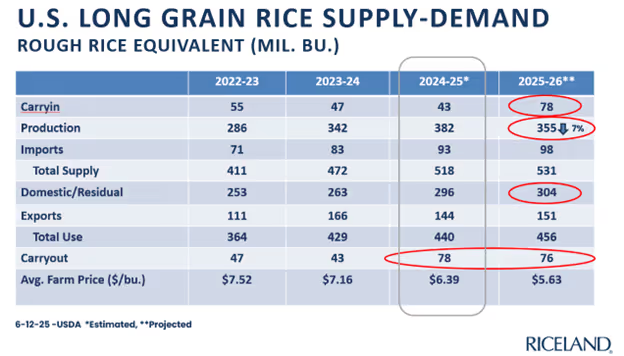

- USDA June 12 WASDE made only small changes to the old crop and a few more changes to new crop. Long Grain acres were reduced a small amount; however, much larger cuts are anticipated for the July 11 WASDE after the June 30 Acreage report is released.

- WASDE may still be too high on new crop domestic use/residual at 304 million bushels.

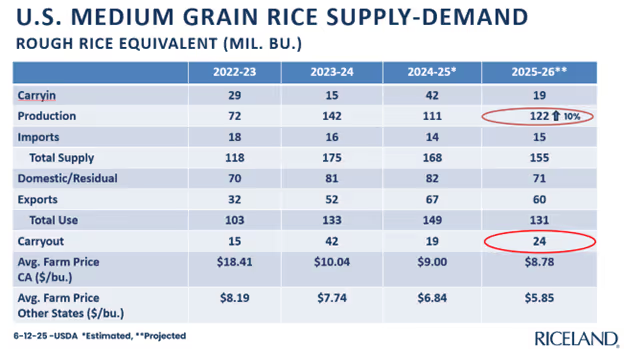

- WASDE showed overall Medium Grain production to be up 10% compared to 2024, due to increased acres in California.

- Medium Grain ending stocks for 25/26 are projected to increase to 24 million bushels, up from 19 million bushels estimated for the current year.

- USDA continues to forecast higher imports for both long and medium grain.

- Long grain rough rice exports continue to drastically lag year-ago levels.

- Long grain milled rice exports are down slightly compared to year-ago levels.

- World rice stocks are projected to be ample, forecast at 188 million metric tons, up slightly from the current year.

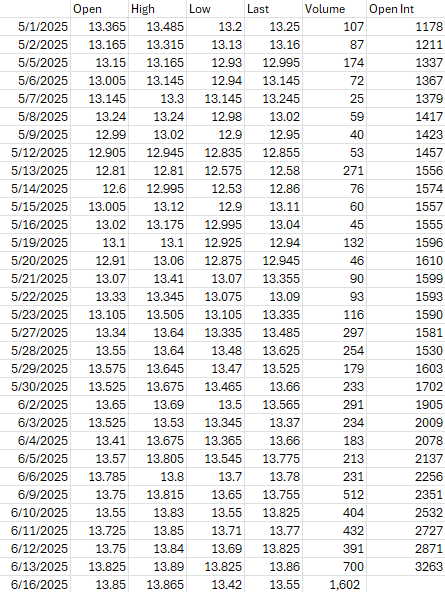

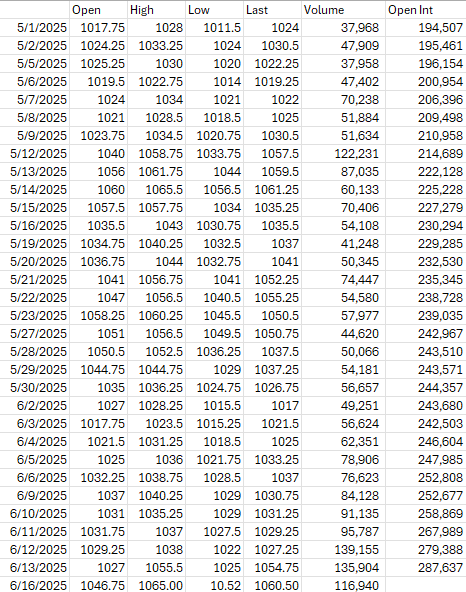

September ’25 Rough Rice Futures

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT September ’25 Rough Rice Values, 5/1/25 through 6/16/25

U.S. Long Grain Rice Supply-Demand

U.S. Medium Grain Rice Supply-Demand

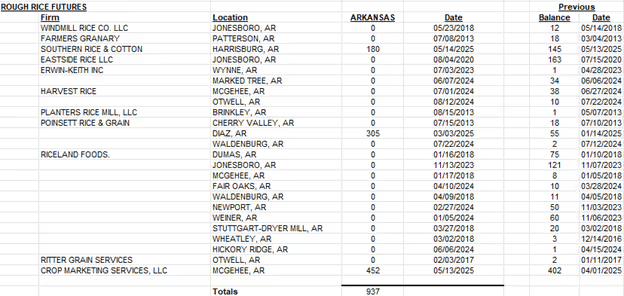

CBOT Receipts As of 6-12-25

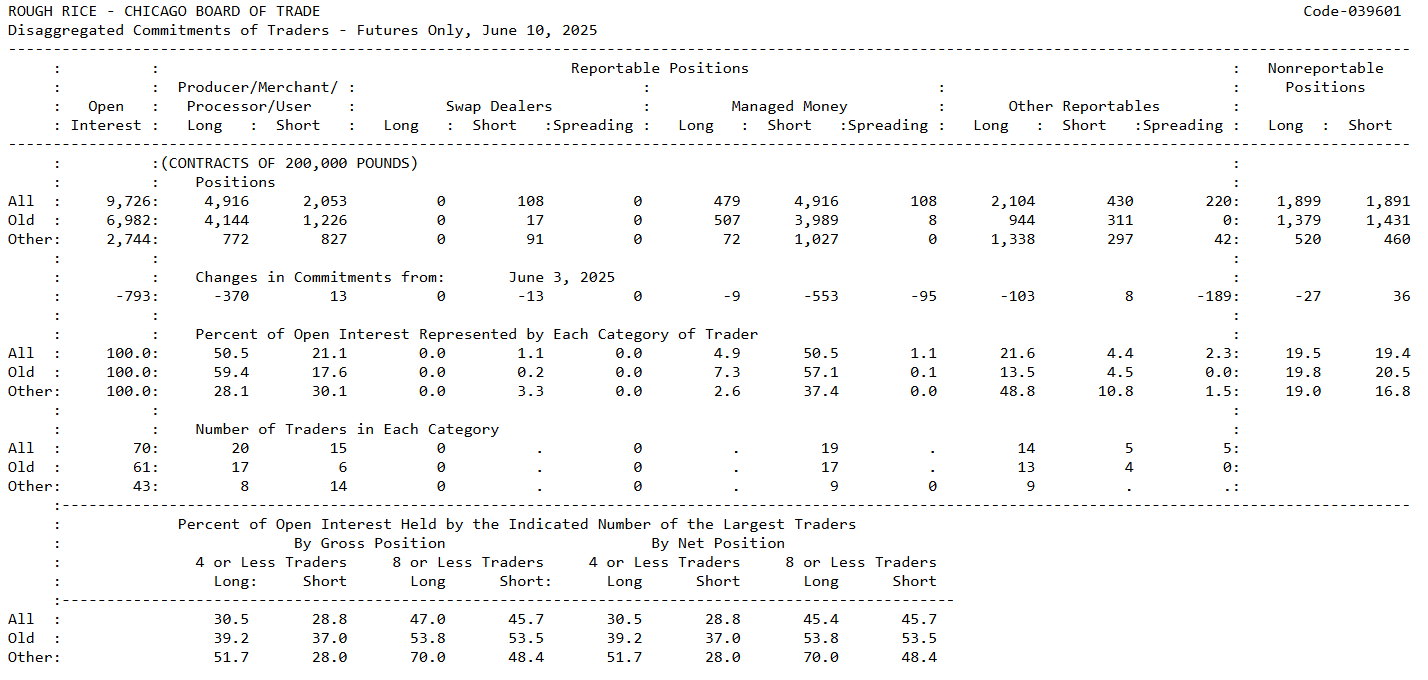

CTFC Commitment of Traders

Rice Market Summary

OLD CROP:

CBOT July ’25 rice futures hit a low of $12.275 on 5/14/25 and quickly bounced back to $13.50 on 5/28/25, and in recent days has traded mostly between $13.40 and $13.75. Milled rice prices in most areas of the world have decreased in recent weeks; however, focus is shifting to new crop and the significant drop in production expected for long grain.

CBOT receipts stand at 937 as of 6/12/25, all in McGehee, Diaz, and Harrisburg.

NEW CROP:

September futures have picked up in volume as traders switch out of their July positions. Prices bottomed on 5/14 and have increased significantly as traders have gotten more nervous about the drop in new crop production. The June 30 Acreage Report will be more important than usual given the uncertainty on prevent plant acreage due to the extremely wet spring.

Soybean Fundamental Highlights

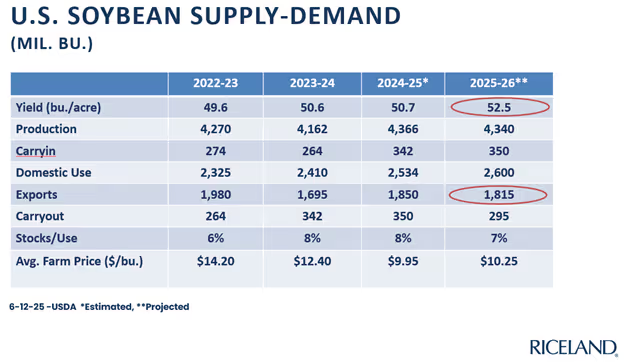

- The June 12 Supply and Demand report from USDA left all soybean numbers unchanged from May.

- The projected average price for new crop remained at $10.25 and ending stocks remained at 295 million bushels.

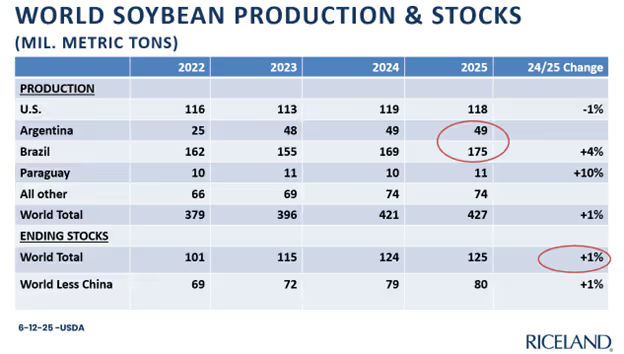

- World soybean stocks are projected to remain nearly flat after a few years of significant increases.

- The soybean market rallied on 6/13 and 6/16 after EPA released much larger RVOs for biofuel which will stimulate demand for soybean oil.

- Traders will be focused on U.S. weather and tariff/trade developments with China, Mexico, and E.U. in the coming weeks.

November ’25 Soybeans

Key:

Orange Line: 9-day moving average

Blue Line: 27-day moving average

CBOT November ’25 Soybean Values, 5/1/25 through 6/16/25

U.S. Soybean Supply-Demand

World Soybean Production & Stocks

Soybean Market Summary

OLD CROP:

July futures have traded mostly between 10.35 and 10.70 in recent days, supported by the bullish RVO numbers released by the EPA on 6/13/25. Even though the EPA volumes are proposed and won’t be finalized until November, they were much higher than the trade expected causing a rally in soybeans and soybean oil, although soybean meal futures have declined.

NEW CROP:

The June 12 USDA WASDE soybean projections for new crop remained the same as the May report which were bullish with ending stocks projected at 295 million bushels. The projection for exports was 1.815 billion bushels, which could be a bit high depending on how the Chinese tariffs wind up affecting trade. With the smaller U.S. crop, weather risk will help to counter the export risk as USDA plugged in 52.5 for the new crop yield which could easily be 1-2 bushels per acre too high unless weather is ideal all summer.

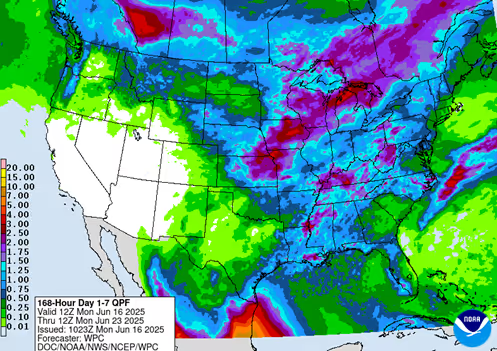

Weather Outlook

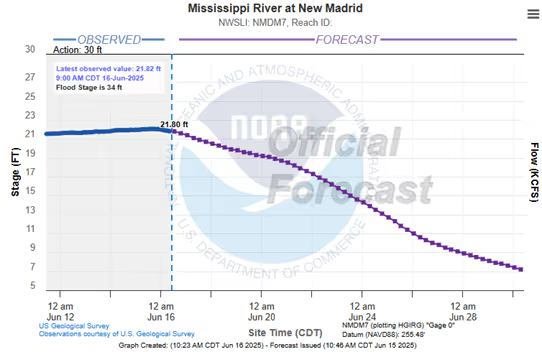

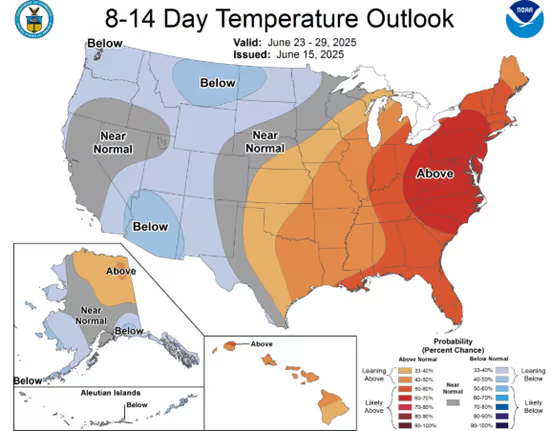

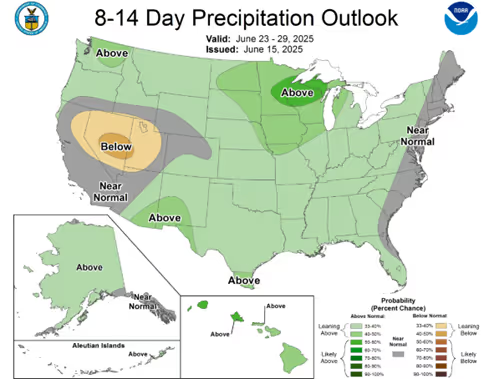

The Mississippi River and Ohio River graphs show receding levels after recent rain events, which should allow normal navigation/shipping for the next several weeks. The near-term precipitation outlook shows more rain for Eastern Arkansas. Amounts are lighter than previous weeks and the higher temps should speed drying. The 8–14-day precipitation outlook shows to be slightly above normal in late June with above normal temperatures.

NOAA Temperature General Outlook

NOAA Precipitation General Outlook

NWS 7-Day Precipitation Outlook